- Details

- Category: Tax advisory

- Hits: 77

Accounting Bogotá

New 2026 rates for Bogotá’s SIMPLE regime

Increase in ICA in Bogotá for SIMPLE regime taxpayers in 2026.

Key information

For 2026, Bogotá increased the ICA component rates for taxpayers registered under the Simple Taxation Regime.

The change was established in Article 44 of Bogotá Council Agreement 1019 of 2025 and applies to the fiscal year from January 1 to December 31, 2026.

It is important to clarify that not all SIMPLE taxpayers are subject to a rate of 30 per thousand. The rate depends on the economic activity group established in Article 908 of the Tax Code.

Previous and new rates

Previously, under Agreement 780 of 2020, Bogotá applied SIMPLE ICA rates between 5 and 12 per thousand, depending on whether the activity was industrial, commercial or service-based.

For 2026, the new rates are:

| SIMPLE Group | Main activities | Approximate previous rate | New 2026 rate |

|---|---|---|---|

| Group 1 | Small stores, minimarkets and hair salons | 6 to 12 per thousand | 12 per thousand |

| Group 2 | Commerce, industry, technical services, construction and other activities | 5 to 12 per thousand | 16 per thousand |

| Group 3 | Sale of food and beverages, and transportation | 6 to 12 per thousand | 30 per thousand |

| Group 3 SIC | Professional services, consulting and liberal professions | 6 to 12 per thousand | 30 per thousand |

| Group 6 | Recycling, material recovery and waste collection | Up to 12 per thousand | 16 per thousand |

Most affected sectors

The most affected sectors are those moving to the 30 per thousand rate, especially:

Restaurants, cafés and establishments selling food and beverages.

Transportation.

Professional services.

Consulting.

Liberal professions.

The impact may be significant because some taxpayers who previously paid between 6 and 12 per thousand would now pay 30 per thousand for the ICA component in Bogotá.

For example, on taxable income of $100,000,000:

| Rate | Approximate ICA on $100,000,000 |

|---|---|

| 12 per thousand | $1,200,000 |

| 30 per thousand | $3,000,000 |

The difference would be $1,800,000 for every $100,000,000 of taxable income in Bogotá.

Recommendations

SIMPLE taxpayers in Bogotá should:

Review which group under Article 908 of the Tax Code they are classified in.

Verify whether all their income actually corresponds to Bogotá or whether part of the activity is carried out in other municipalities.

Simulate whether remaining under the SIMPLE regime continues to be convenient.

Adjust budgets, advances and prices for 2026.

Avoid changing the economic activity only to seek a lower rate if it does not correspond to the business reality.

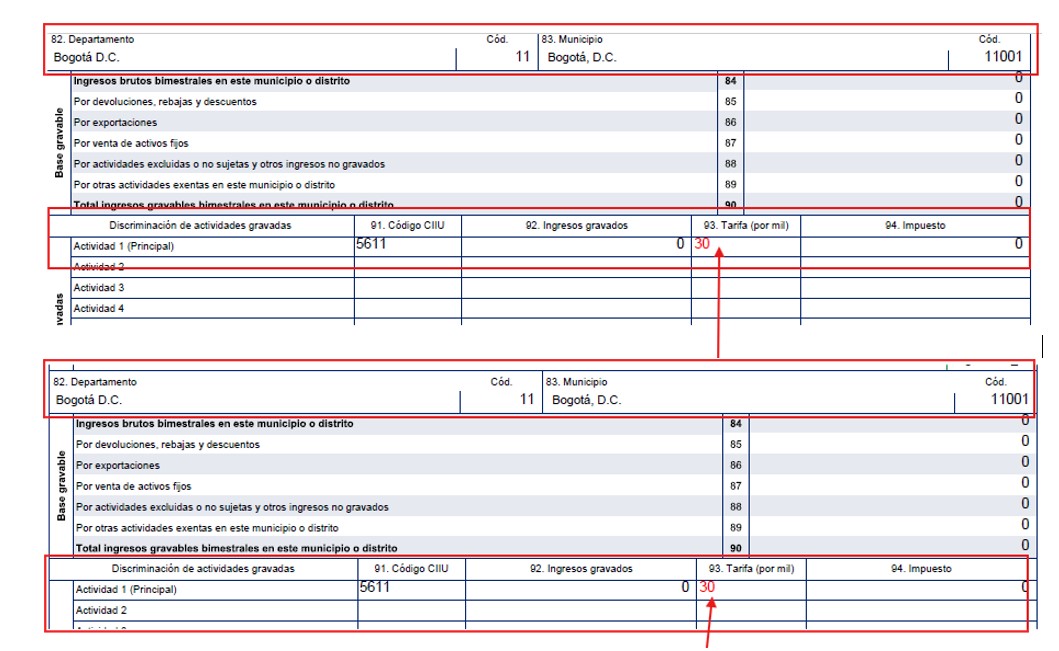

In advances filed for the January-February 2026 bimonthly period, the 30 per thousand rate is shown for activity 5611, restaurant services, and activity 7020, consulting services, which are among the most affected by this increase.

Through Press Release 074 of May 19, 2026, the DIAN clarified that the increase in Bogotá’s consolidated ICA component does not mean that the national rates of the Simple Taxation Regime increased.

What happened is that Bogotá, through District Agreement 1019 of 2025, increased the consolidated ICA component rate for some SIMPLE taxpayers, especially those in group 3 and group 3 SIC, from 10 per thousand to 30 per thousand. These groups mainly include the sale of food and beverages, transportation, professional services, consulting and scientific activities.

So did SIMPLE increase?

Not necessarily. According to the DIAN, the general SIMPLE rate was not increased by the National Government. What changes is the internal distribution of the tax.

The SIMPLE regime is made up of several elements, including:

The national SIMPLE component, administered by the DIAN.

The territorial ICA component, which belongs to the municipality or district.

When Bogotá’s ICA component increases, the portion corresponding to the national SIMPLE component decreases. Therefore, the DIAN indicated that the change does not increase the total value of the RST advance; it represents an internal redistribution among the components of the consolidated tax.

Practical example

Suppose a group 3 taxpayer in Bogotá has bimonthly income of $100,000,000 and a consolidated SIMPLE rate of 3.4%.

| Concept | Before the Bogotá ICA increase | After the Bogotá ICA increase |

|---|---|---|

| Taxpayer’s bimonthly income | $100,000,000 | $100,000,000 |

| SIMPLE regime group | Group 3 | Group 3 |

| Consolidated SIMPLE rate in the example | 3.40% | 3.40% |

| Total SIMPLE tax | $3,400,000 | $3,400,000 |

| Bogotá ICA rate | 10 per thousand | 30 per thousand |

| Bogotá ICA component | $1,000,000 | $3,000,000 |

| National DIAN component | $2,400,000 | $400,000 |

| Total payable on the SIMPLE receipt | $3,400,000 | $3,400,000 |

Conclusion

The increase in SIMPLE ICA in Bogotá for 2026 is real, but it does not apply equally to everyone. The rates are 12, 16 or 30 per thousand, depending on the activity group.

The greatest impact will fall on taxpayers providing professional services, consulting, restaurants, food establishments and transportation, which are subject to the 30 per thousand rate.

It cannot be said that the SIMPLE tax in general increased. The correct statement is that, in Bogotá, the consolidated ICA component increased for certain groups within the SIMPLE regime.

Consequently, the general SIMPLE rate remains the same, but the distribution of the payment changes: Bogotá receives a larger share through ICA and the DIAN receives a smaller share through the national component.

For some taxpayers who already filed the SIMPLE advance for the January-February 2026 bimonthly period, this increase was not reflected.

If you have comments, contact us.

If this information helped you, leave us your comments here.We provide tax advisory services..

Contact us: WhatsApp 310 558 91 17 - 313 821 48 03

If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step.

- Details

- Category: Tax advisory

- Hits: 72

Accounting Bogotá

I received a letter, email or request from the DIAN

I received a letter, email or request from the DIAN. What should I do?

Key information

First, attention must be paid to requests made by the DIAN. Normally, when this entity finds that a taxpayer must comply with a tax obligation, it sends a message or invitation to file an income tax return, asking the person to comply with what is requested in the message.

When the DIAN issues these communications, in most cases they must be complied with or answered because the DIAN has performed the corresponding information cross-checks to determine whether the person is required to comply with one or more obligations.

If you received a physical letter, an email message or even a text message to your cell phone, the most advisable course is to contact us so we can determine the authenticity of the message and tell you the steps to follow. It is very important to emphasize that at the first notification it is better to act immediately. If you do not respond, the DIAN continues notifying you through its legal procedure, making the obligation increasingly expensive to comply with.

For example, if you are required to file an income tax return, it is better to do so. In many cases the tax payable is zero, but the penalty for not filing or for filing late in 2026 is $524,000.

The consultation with us to determine your obligation is free.

Phone: 310 558 91 17 - 313 821 48 03, or submit your inquiry through this page.

- Details

- Category: Tax advisory

- Hits: 56

Accounting Bogotá

Tax and Fiscal Advisory

Review obligations, returns and taxes by topic.

- Details

- Category: Tax advisory

- Hits: 60

Accounting Bogotá

Determine National and Local Tax Obligations

Carrying out a business activity or providing income-generating services implies national and local tax responsibilities. It is important to identify the obligations that apply in order to avoid possible investigations, penalties and late-payment interest costs. Acquiring these tax responsibilities does not necessarily mean that the consequence will be paying taxes. Identifying in time which responsibilities arise from carrying out business activities is essential to reduce unbudgeted and unexpected costs. A request from a tax authority such as the DIAN or a municipal or local tax office can be exhausting, frustrating, costly, and may even seriously affect your personal assets. In many cases, several years may pass without any type of request. Tax authorities may let time pass, sometimes deliberately, and act during the final period legally available to them in order to secure higher revenue. These entities usually have up to five years to begin a process that may end in collection for all years that were not declared.

Would you like to pay less income tax to the DIAN and less Industry, Commerce and Signage Tax (ICA)?

For 2022, 2023 and subsequent years, the rate used to calculate tax in income tax returns for both individuals and legal entities in Colombia is 35%. In addition to the above, ICA tax must be paid on the income received, and the rate depends on each municipality. These taxes represent a very high tax burden, especially for small companies and merchants, as well as for some professionals who work independently.

By registering under the Simple Taxation Regime (Régimen Simple de Tributación, RST), the burden of complying with tax obligations is not only simplified; most importantly, the amount payable as taxes may be significantly reduced because the rates are much lower. RST rates range from 1.8% to 14.5%, and their application depends on gross income and the business activity carried out.

Contact us and we will help you evaluate the possibility of reducing your tax payments.

Remember: the first consultation is FREE. Request it here.If you need more information, advice or guidance, request an appointment here or write to

310 558 91 17 – 313 821 48 03Supporting Document for purchases made from parties not required to issue invoices.

Do you know whether you must generate a Supporting Document for purchases made from parties not required to issue invoices?

According to DIAN Resolution 167 of December 30, 2021, the required parties had a deadline to implement it beginning May 2, 2022. However, through Resolution 488 of April 29, 2022, the DIAN postponed this obligation to August 1, 2022. Nevertheless, as with Electronic Invoicing and Electronic Payroll, this Supporting Document is already a reality, so implementation is necessary.

But who is required to do it?

You are required to generate it if you acquire goods or services, when you make purchases or obtain services from a supplier that is not required to issue a sales invoice, so that you can document the transaction and have the support for costs, deductions or deductible taxes in your tax returns.

If you are an electronic invoicer, VAT-liable party, income tax and complementary tax taxpayer, and you need to support costs and deductions for income tax and complementary tax purposes, as well as deductible VAT, you must generate the Supporting Document.

Do you need more information? Request an appointment or contact us here or at:

310 558 91 17 - 313 821 48 03

Tax Value Unit (UVT) value, year 2026

Through Resolution 000238 of December 15, 2025, the DIAN set the value of the Tax Value Unit (UVT) applicable in 2026.

Concept | 2026 Value

Tax Value Unit (UVT) | $52,374

Minimum penalty | $524,000

| These values are used for different calculations in the assessment of taxes and penalties for omission or late filing. | As a business owner, you should focus your efforts on developing your company’s operations. We take care of the accounting, financial information, correct tax calculation and timely filing of taxes so that you do not incur unnecessary penalties. |

|---|---|

| Remember that we treat your accounting matter, situation or problem as our own in order to solve it quickly. | Contact us: +57 310 558 91 17 – 313 821 48 03 |

| Schedule your appointment for more personalized advice here. | New ICA rates in Bogotá as of 2022 |

With the issuance of District Agreement 780 of November 6, 2020, new rates were created for the Industry and Commerce Tax (ICA) in the city of Bogotá.

Article 6 of the Agreement modifies the Industry and Commerce Tax rate, starting in taxable year 2022, for industrial, service and financial activities. Among others, professional consulting activities and services provided by contractors, builders and developers increased from 6.9 to 8.66 per thousand, while consulting services in the practice of a liberal profession decreased from 9.66 to 7.66 per thousand as of 2022.

Likewise, Article 5 establishes a temporary increase in ICA rates for taxable year 2021 for those who increased their income during the epidemiological situation caused by Coronavirus (COVID-19).

Later, Resolution No. SDH-000265 of April 13, 2021 adopted and updated the classification of economic activities (CIIU) and defined the ICA rates for all taxable activities in Bogotá.

For the correct application of Bogotá’s Industry and Commerce Tax, the District Treasury Secretariat (SDH) has published the ICA Guide, which undoubtedly helps clarify several questions when applying the tax.

These rates are important in order to apply the correct rate in ICA withholding processes. Learn here who the withholding agents are for Bogotá’s Industry and Commerce Tax and how the system operates.

According to the dynamics of how ICA withholding operates among taxpayers under Article 2, “Operation of the System,” of Resolution DDI-000305 of January 16, 2020 on withholding agents, Bogotá’s ICA Large Taxpayers are subject to withholding only by public entities and by large taxpayers designated by the DIAN. For 2026, Resolution DDI 029334 of October 31, 2025 designated Bogotá’s ICA Large Taxpayers.

(1 Section taken from...) “The withholding system is governed, as applicable to the nature of the Industry and Commerce Tax, by the specific rules adopted by the Capital District and the general withholding system rules applicable to income tax and complementary taxes.

To ensure efficient collection of the Industry and Commerce Tax, the Bogotá District Tax Directorate, based on Agreements 65 of 2002 and 756 of 2019, issued Resolution DDI-000305 of January 16, 2020, through which withholding agents for the Industry and Commerce Tax are designated.

The following are withholding agents:

Public law entities.

Those classified as large taxpayers by the National Tax and Customs Directorate (DIAN).

Those designated as withholding agents for the Industry and Commerce Tax by resolution of the district tax director.

Intermediaries or third parties that participate in economic operations in which Industry and Commerce Tax withholding is generated, in accordance with the regulations.

Consortiums and temporary unions shall be Industry and Commerce Tax withholding agents when they make payments or credits to account whose beneficiaries are taxpayers under the ordinary ICA regime and/or the preferential ICA regime, in transactions taxed with ICA within the jurisdiction of the Capital District.

Industry and Commerce Tax taxpayers belonging to the ordinary regime must apply withholdings whenever the payment beneficiary is a taxpayer belonging to the preferential regime, in accordance with the terms established in Article 10 of Agreement 756 of 2019, and carries out transactions for activities taxed with the tax within the jurisdiction of the Capital District.

As of July 1, 2004, Industry and Commerce Tax taxpayers belonging to the ordinary regime must apply Industry and Commerce withholding to payment beneficiaries or credits to account registered under the ordinary regime if they are independent professionals, when they participate in transactions for activities taxed with the tax within the jurisdiction of the Capital District of Bogotá.

Circumstances under which withholding is NOT applied:

Payments or credits to account made to non-ICA taxpayers.

Payments or credits to account that are not subject to tax or are exempt.

When the beneficiary of the payment is a public law entity.

When the beneficiary is classified as a large taxpayer by the DIAN and is an ICA filer in Bogotá, except when the withholding agent is a public entity.

Resources from the capitation payment unit of the subsidized and contributory regimes of the General Social Security Health System.

Payments for public utilities.

If there is a special taxable base, the withholding is applied on that base.

The Industry and Commerce Tax withholding rate shall be the rate corresponding to the respective activity. When the party subject to withholding does not report the activity or the activity cannot be established, the withholding rate shall be the maximum rate in force for the Industry and Commerce Tax within the taxable period, and the transaction shall be taxed at that same rate.”

Minimum bases to apply withholding for 2026:

Minimum withholding bases for 2026 (UVT value: $52,374)

Concept | Base in UVT | Base in pesos

Services | 4 UVT | $209,496

Purchases | 27 UVT | $1,414,098

(1) Source: Bogotá District Treasury Secretariat - ICA.

If this information helped you, leave us your comments here.

We provide tax advisory services.

| Expiration of DIAN electronic signature | Expiration of DIAN Electronic Signature. | The Electronic Signature replaced what was formerly called the Digital Signature. This mechanism is used by the DIAN to validate the information submitted by taxpayers. In this way, the tax authority ensures that the documents are generated directly by the responsible parties, that there is no impersonation, and therefore that the information has full legality and effectiveness. This mechanism was implemented in 2016. |

|---|---|---|

| Because this mechanism is valid for three (3) years, it is very possible that for some taxpayers who processed it, it has already expired or is close to expiring. As a result, they may have problems signing documents for submission to the DIAN and may fall into late filing of tax obligations such as withholding tax, according to the 2020 tax calendar and the modifications made because of the state of emergency declared by the National Government due to the global situation related to COVID-19. | Solution | If it has not yet expired, the update procedure is very simple and can be completed online (see the step-by-step guide): https://www.dian.gov.co/impuestos/Firma%20Electrnica/1pasoapaso.pdf. However, if it has already expired, the process is somewhat more complex, especially considering mobility restrictions, since this procedure normally must be carried out in person. Nevertheless, for now this service can be handled online by requesting an appointment with the DIAN at https://agendamientodigiturno.dian.gov.co/ and following the process, which may take several days. |

| If you need help or guidance, we will gladly assist you. | Contact us by email here or by phone at 313 821 48 03 – 310 558 91 17. The first consultation is FREE. | Value Added Tax (VAT) Advisory |

Advisory services on Value Added Tax (VAT) for people who start a business activity or provide services and, when registering in the RUT, seek to be classified as not responsible for VAT (formerly the Simplified Regime), in order not to become responsible for Value Added Tax. However, even if they meet the legal requirements, doing so may cause them to lose many business opportunities because of the limitations this regime imposes.First, it limits business growth and development. The purpose of starting a business is to achieve the fastest possible growth. However, although being classified as not responsible for VAT under obligation 49 in the RUT reduces obligations, it also significantly limits proper business development..

If you register under obligation 49 — Not responsible for VAT — you are setting limits on growth and development. By contrast, being classified under responsibility 48 — Sales Tax — not only considerably expands the field of action in business and avoids limiting growth out of fear of being reclassified, but the amounts payable as VAT may be minimal compared with the business development that can be achieved. For this, it is enough to comply with the filing deadlines according to the DIAN tax calendar for 2022.The obligation to invoice is independent of VAT responsibility; therefore, a person may not be responsible for VAT and at the same time may be required to issue invoices. This is established by Unified Electronic Invoice Concept 100202208-106-RAD-91142 of August 19, 2022..

The first advisory session is FREE.

310 558 91 17 - 313 821 48 03

The DIAN requires independent professionals, salaried employees and restaurants

Within the “Up to Date with the DIAN” program, the DIAN carries out visits and other procedures for independent professionals, salaried employees and restaurants in order to encourage compliance with their obligations.

The tax authority estimates that many people, especially independent workers, do not comply with their tax obligations and may therefore be considered non-filers or evaders.

It should be remembered that the DIAN currently has sufficient mechanisms to identify taxpayers who fail to comply with their obligations and who may be required to respond at any time.

Frequently, when the DIAN issues a request, it is because it has sufficient information about the taxpayer. The best thing that taxpayer can do is pay proper attention to the request and find a way to become “up to date with the DIAN.” However, taxpayers should not forget that they may incur possible penalties, which in many cases are much higher than the taxes themselves.

Consequently, if you believe you have pending matters with the DIAN, it is better to act in time. Contact us and we will guide you through these procedures. Phone: 310 558 91 17. The first consultation is free.

https://www.dian.gov.co/descargas/EscritosComunicados/2017/170_Comunicado_de_prensa_27102017.pdf

National Consumption Tax (INC)

Restaurants, cafés, fruit shops, bakeries, fast-food outlets, bars, taverns and nightclubs have a defined regime regarding value added tax. These activities are generally not required to charge VAT, except in specific cases, but are subject to the National Consumption Tax (INC).

The simplified and ordinary INC regimes also apply to them. In both cases, those who carry out these activities have obligations, and non-compliance leads to penalties. Many of the businesses mentioned fail to comply with the minimum legal operating guidelines and are therefore exposed to possible fines or penalties. By formalizing your business, you gain an advantage over others because you can focus on its growth without fear. Proper classification under the correct regime ensures the normal development of activities without creating additional burden.

With our advice, we identify whether you fall under the ordinary or simplified regime of the National Consumption Tax (INC), clearly indicating the advantages and disadvantages in each case and proposing viable alternatives. We always seek compliance with tax regulations, while also seeking the maximum legally permitted reduction of costs in pursuit of a fair balance.

Obligations, DIAN, ICA and compliance

I received a letter, email or request from the DIAN.

Just like your best friend, government entities know many things about you.

The DIAN requires independent professionals, salaried employees and restaurants.

Solution to the “Invalid Validity / Number of Columns” error in Bogotá district magnetic media.

Expiration of DIAN electronic signature.

New ICA rates in Bogotá as of 2022.

Tax Value Unit (UVT) value, year 2026.

Would you like to pay less income tax to the DIAN and less Industry, Commerce and Signage Tax (ICA)?

New 2026 rates for Bogotá’s SIMPLE regime.

If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step.

Schedule an appointment

General contact

También les aplica el Régimen Simplificado y el Común del INC. En ambos casos los ejecutores de estas actividades tienen unas obligaciones cuyo incumplimiento deriva en sanciones. Muchos de los negocios mencionados incumplen los mínimos lineamientos legales de funcionamiento por lo que están expuestos a eventuales multas o sanciones. Al formalizar su negocio tienen ventaja frente a los demás ya que se pueden concentrar en el crecimiento del mismo sin temor alguno. Una adecuada clasificación del régimen asegura un desarrollo normal de actividades sin que implique mayor desgaste.

Con nuestra asesoría se identifica si usted aplica al Régimen Común o Simplificado del Impuesto Nacional al Consumo INC indicándole de forma clara las ventajas y desventajas en cada caso proponiendo alternativas viables buscando siempre el cumplimento de la norma tributaria pero buscando también la reducción de los costos al máximo permitido en la búsqueda de un justo equilibrio