- Details

- Category: Tax advisory

- Hits: 58

Accounting Bogotá

Preparation of Tax Returns

Choose the return or tax topic you would like to review.

- Details

- Category: Tax advisory

- Hits: 73

Accounting Bogotá

Income Tax Return Advisory

Our income tax return advisory service, including the requirements for 2025-2026, allows us to identify the tax and fiscal obligations that apply and that, if unknown, may lead to non-compliance with formal and substantive obligations. Formal obligations refer to the duties that must be fulfilled in order to comply with substantive obligations. Examples of formal obligations include registration in the RUT, registration in the Tax Information Registry (RIT), and similar duties. Substantive obligations include, for example, filing income tax, VAT, ICA and other returns.

Income Tax Return Advisory

These returns have minimum requirements to ensure their effectiveness, that is, to be considered properly filed. Otherwise, the return may be deemed ineffective, generating penalties and interest, which in many cases may be higher than the tax itself.

Proper advisory support can help you avoid excessive tax payments, penalties and interest.

For 2026, the DIAN minimum penalty is 10 UVT, that is, $524,000. For example, a return with $10,000 of tax payable, if not filed correctly, may turn into an amount payable greater than $524,000. For this purpose, the filing deadlines under the DIAN 2026 tax calendar must be taken into account.

Request advice with no obligation here, schedule an advisory appointment here, call 310 558 91 17, or check whether you must file an income tax return here.

New 2026 rates for Bogotá’s SIMPLE regime

Increase in ICA in Bogotá for SIMPLE regime taxpayers in 2026.

For 2026, Bogotá increased the ICA component rates for taxpayers registered under the Simple Taxation Regime.

The change was established in Article 44 of Bogotá Council Agreement 1019 of 2025 and applies to the fiscal year from January 1 to December 31, 2026.

It is important to clarify that not all SIMPLE taxpayers are subject to a rate of 30 per thousand. The rate depends on the economic activity group established in Article 908 of the Tax Code.

Previous and new rates

Previously, under Agreement 780 of 2020, Bogotá applied SIMPLE ICA rates between 5 and 12 per thousand, depending on whether the activity was industrial, commercial or service-based.

For 2026, the new rates are:

| SIMPLE Group | Main activities | Approximate previous rate | New 2026 rate |

|---|---|---|---|

| Group 1 | Small stores, minimarkets and hair salons | 6 to 12 per thousand | 12 per thousand |

| Group 2 | Commerce, industry, technical services, construction and other activities | 5 to 12 per thousand | 16 per thousand |

| Group 3 | Sale of food and beverages, and transportation | 6 to 12 per thousand | 30 per thousand |

| Group 3 SIC | Professional services, consulting and liberal professions | 6 to 12 per thousand | 30 per thousand |

| Group 6 | Recycling, material recovery and waste collection | Up to 12 per thousand | 16 per thousand |

Most affected sectors

The most affected sectors are those moving to the 30 per thousand rate, especially:

Restaurants, cafés and establishments selling food and beverages.

Transportation.

Professional services.

Consulting.

Liberal professions.

The impact may be significant because some taxpayers who previously paid between 6 and 12 per thousand would now pay 30 per thousand for the ICA component in Bogotá.

For example, on taxable income of $100,000,000:

| Rate | Approximate ICA on $100,000,000 |

|---|---|

| 12 per thousand | $1,200,000 |

| 30 per thousand | $3,000,000 |

The difference would be $1,800,000 for every $100,000,000 of taxable income in Bogotá.

Recommendations

SIMPLE taxpayers in Bogotá should:

Review which group under Article 908 of the Tax Code they are classified in.

Verify whether all their income actually corresponds to Bogotá or whether part of the activity is carried out in other municipalities.

Simulate whether remaining under the SIMPLE regime continues to be convenient.

Adjust budgets, advances and prices for 2026.

Avoid changing the economic activity only to seek a lower rate if it does not correspond to the business reality.

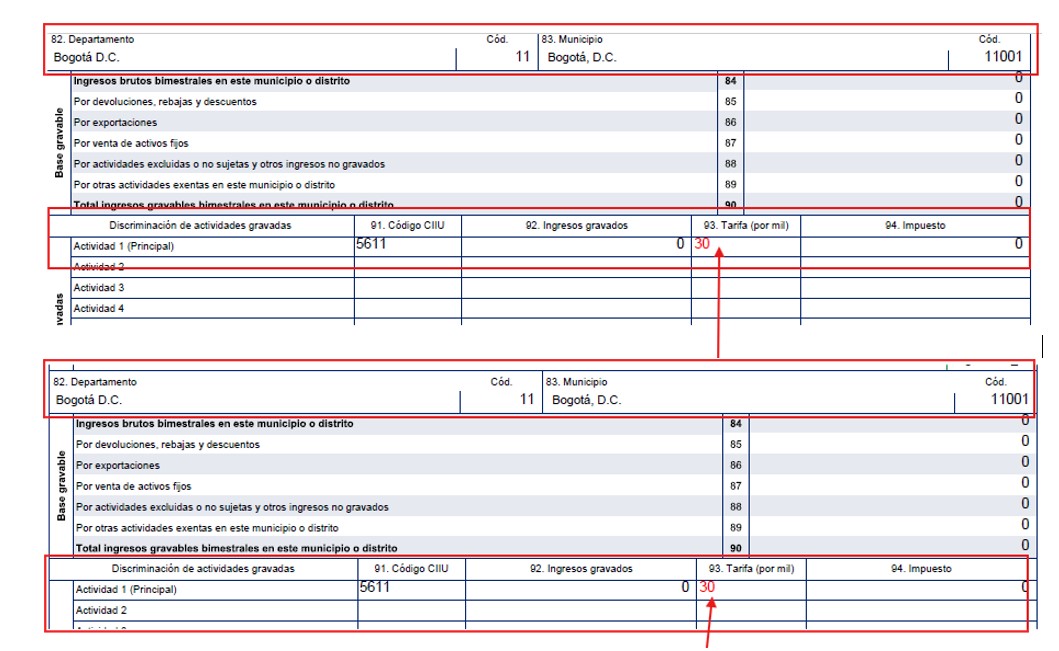

The images of two advances filed for the January-February 2026 bimonthly period show the 30 per thousand rate for activity 5611, restaurant services, and activity 7020, consulting services, which are among the most affected by this increase.

Through Press Release 074 of May 19, 2026, the DIAN clarified that the increase in Bogotá’s consolidated ICA component does not mean that the national rates of the Simple Taxation Regime increased.

What happened is that Bogotá, through District Agreement 1019 of 2025, increased the consolidated ICA component rate for some SIMPLE taxpayers, especially those in group 3 and group 3 SIC, from 10 per thousand to 30 per thousand. These groups mainly include the sale of food and beverages, transportation, professional services, consulting and scientific activities.

So did SIMPLE increase?

Not necessarily. According to the DIAN, the general SIMPLE rate was not increased by the National Government. What changes is the internal distribution of the tax.

The SIMPLE regime is made up of several elements, including:

The national SIMPLE component, administered by the DIAN.

The territorial ICA component, which belongs to the municipality or district.

When Bogotá’s ICA component increases, the portion corresponding to the national SIMPLE component decreases. Therefore, the DIAN indicated that the change does not increase the total value of the RST advance; it represents an internal redistribution among the components of the consolidated tax.

Practical example

Suppose a group 3 taxpayer in Bogotá has bimonthly income of $100,000,000 and a consolidated SIMPLE rate of 3.4%.

| Concept | Before the Bogotá ICA increase | After the Bogotá ICA increase |

|---|---|---|

| Taxpayer’s bimonthly income | $100,000,000 | $100,000,000 |

| SIMPLE regime group | Group 3 | Group 3 |

| Consolidated SIMPLE rate in the example | 3.40% | 3.40% |

| Total SIMPLE tax | $3,400,000 | $3,400,000 |

| Bogotá ICA rate | 10 per thousand | 30 per thousand |

| Bogotá ICA component | $1,000,000 | $3,000,000 |

| National DIAN component | $2,400,000 | $400,000 |

| Total payable on the SIMPLE receipt | $3,400,000 | $3,400,000 |

Conclusion

The increase in SIMPLE ICA in Bogotá for 2026 is real, but it does not apply equally to everyone. The rates are 12, 16 or 30 per thousand, depending on the activity group.

The greatest impact will fall on taxpayers providing professional services, consulting, restaurants, food establishments and transportation, which are subject to the 30 per thousand rate.

It cannot be said that the SIMPLE tax in general increased. The correct statement is that, in Bogotá, the consolidated ICA component increased for certain groups within the SIMPLE regime.

Consequently, the general SIMPLE rate remains the same, but the distribution of the payment changes: Bogotá receives a larger share through ICA and the DIAN receives a smaller share through the national component.

For some taxpayers who already filed the SIMPLE advance for the January-February 2026 bimonthly period, this increase was not reflected.

If you have comments, contact us.

If this information helped you, leave us your comments here.We provide tax advisory services..

Contact us; the first consultation is free: Tel / WhatsApp 310 558 91 17 – 313 821 48 03

Income tax return calendar for individuals, taxable year 2025

If you are required to file your income tax return for taxable year 2025, which is filed in 2026 according to the last two digits of your NIT or citizenship ID number, the following are the maximum dates for filing the corresponding return. Remember, however, that preparing the return takes time and must be done with special care, without rushing. Therefore, it is recommended to begin the process now in coordination with your accountant and have it ready at least three days before the deadline.

Who must file an income tax return for 2025 starting August 12, 2026.

Individuals not required to file an income tax return in 2026 for taxable year 2025.

All individuals and estates that meet the following conditions are not required to file an income tax return for taxable year 2025.

To avoid being required to file an income tax return for taxable year 2025, all these conditions must be met:

Condition | Limit or requirement

| Not being responsible for VAT | Qualitative requirement |

|---|---|

| Gross assets at the end of the taxable year | Up to 4,500 UVT ($224,096,000) |

| Gross income | Less than 1,400 UVT ($69,719,000) |

| Credit card consumption | Up to 1,400 UVT ($69,719,000) |

| Total purchases and consumption | Up to 1,400 UVT ($69,719,000) |

| Bank deposits, deposits or financial investments | Up to 1,400 UVT ($69,719,000) |

| Minimum late-filing penalty | $524,000 |

| If you do not meet any of the above conditions, you must file the income tax return for 2025. | Documents required to prepare the income tax return for taxable year 2025. |

In coordination with your accountant, you must provide the following documents, among others, as a basis for preparing the income tax return:

A copy of the certificate of registration in the Single Tax Registry (RUT), duly updated.

Income tax returns for the last two taxable years.

Documents to determine assets:

Certificates or statements showing the balances of savings and checking accounts issued by financial institutions.

Investment certificates issued by the entities where the investment was made, such as CDs, bonds, trust rights, mandatory investments and others.

Property tax declaration or account statement for real estate owned.

Deeds of acquisition for real estate and/or certificates from the public registry.

Vehicle purchase invoice or document showing the acquisition value of vehicles and vehicle tax account statement.

List of furniture, fixtures, machinery and equipment, at acquisition value plus additions and improvements.

Technical appraisal certificate for intangible assets such as goodwill, copyright, industrial, literary, artistic and scientific property, and others.

Bills of exchange, promissory notes and other documents supporting accounts receivable and obligations or debts, in accordance with legal requirements.

Documents to determine income:

Certificate of employment income and withholdings.

Certificates of compensation for work accidents or illness, maternity, worker burial expenses, death insurance and death compensation for members of the Military Forces and National Police.

Certificates for dividends and shares received during the year.

Certificates for pension substitute indemnities or refunds of pension savings balances.

Certificates of income for fees, commissions and services.

Certificates of financial returns paid during the year, issued by the corresponding entities.

Certificates of dividends and shares received during the year, issued by the companies of which you are a partner or shareholder.

Certificates of income received during the year from profits distributed by liquidated companies.

Certificates of payments for meals made by your employer.

Certificates of payment of life insurance indemnities.

Documents to determine payments that constitute deductions:

Certificate of interest payments on loans for housing acquisition.

Certificates for mandatory health payments and prepaid medical plans.

Certificates for investments in new irrigation plantations, wells, silos, detention centers, maintenance and conservation of audiovisual works, bookstores, film projects and others.

Certificates for donations to the Nation, departments, municipalities, districts, Indigenous territories and others.

List of expense invoices, indicating the total value.

List of payments made to employees for salaries, bonuses, vacation, severance pay and others.

Contact us and we will prepare your return.

Phone: 310 558 91 17 - 313 821 48 03

Withholding Tax

Withholding tax is not a tax in itself; it is a mechanism through which the government collects a tax in advance, that is, before the filing deadline. You may be a withholding agent without knowing it, or withholding may be applied to you and you may not know what to do with it. In any of these cases, it is necessary to understand the reason for the situation in order to ensure proper regulatory compliance and avoid high penalties for non-compliance. If you are a merchant and withholding tax was applied to you, meaning you were paid less, you may not have to lose that amount; we will tell you how to proceed in these cases.

It should be noted that withholding tax must be paid within the corresponding deadlines. If it is not paid, the filing will be considered not made, and therefore it must be filed again and the corresponding penalties and interest must be calculated.

+57 310 558 91 17 - +57 313 821 48 03

If you need more information, advice or guidance, request an appointment here.

Individual income tax and calendar

How to know whether I must file an income tax return.Income tax return calendar for individuals, taxable year 2025.

- Details

- Category: Tax advisory

- Hits: 74

Accounting Bogotá

Withholding Tax

Withholding tax is not a tax in itself; it is a mechanism through which the government collects a tax in advance, that is, before the filing deadline. You may be a withholding agent without knowing it, or withholding may be applied to you and you may not know what to do with it. In any of these cases, it is necessary to understand the reason for the situation in order to ensure proper regulatory compliance and avoid high penalties for non-compliance. If you are a merchant and withholding tax was applied to you, meaning you were paid less, you may not have to lose that amount; we will tell you how to proceed in these cases. It should be noted that withholding tax must be paid within the corresponding deadlines. If it is not paid, the filing will be considered not made, and therefore it must be filed again and the corresponding penalties and interest must be calculated.

Withholding Tax

+57 310 558 91 17 - +57 313 821 48 03

If you need more information, advice or guidance, request an appointment here.New 2026 rates for Bogotá’s SIMPLE regime

Increase in ICA in Bogotá for SIMPLE regime taxpayers in 2026.

For 2026, Bogotá increased the ICA component rates for taxpayers registered under the Simple Taxation Regime.

The change was established in Article 44 of Bogotá Council Agreement 1019 of 2025 and applies to the fiscal year from January 1 to December 31, 2026.

It is important to clarify that not all SIMPLE taxpayers are subject to a rate of 30 per thousand. The rate depends on the economic activity group established in Article 908 of the Tax Code.

Previous and new rates

Previously, under Agreement 780 of 2020, Bogotá applied SIMPLE ICA rates between 5 and 12 per thousand, depending on whether the activity was industrial, commercial or service-based.

For 2026, the new rates are:

SIMPLE Group | Main activities | Approximate previous rate | New 2026 rate

| Group 1 | Small stores, minimarkets and hair salons | 6 to 12 per thousand | 12 per thousand |

|---|---|---|---|

| Group 2 | Commerce, industry, technical services, construction and other activities | 5 to 12 per thousand | 16 per thousand |

| Group 3 | Sale of food and beverages, and transportation | 6 to 12 per thousand | 30 per thousand |

| Group 3 SIC | Professional services, consulting and liberal professions | 6 to 12 per thousand | 30 per thousand |

| Group 6 | Recycling, material recovery and waste collection | Up to 12 per thousand | 16 per thousand |

| Most affected sectors | The most affected sectors are those moving to the 30 per thousand rate, especially restaurants, cafés, food and beverage establishments, transportation, professional services, consulting and liberal professions. | The impact may be significant because some taxpayers who previously paid between 6 and 12 per thousand would now pay 30 per thousand for the ICA component in Bogotá. | For example, on taxable income of $100,000,000: |

Rate | Approximate ICA on $100,000,000

12 per thousand | $1,200,000

30 per thousand | $3,000,000

The difference would be $1,800,000 for every $100,000,000 of taxable income in Bogotá.

Recommendations

SIMPLE taxpayers in Bogotá should review which group under Article 908 of the Tax Code they are classified in, verify whether all income actually corresponds to Bogotá or whether part of the activity is carried out in other municipalities, simulate whether remaining under the SIMPLE regime continues to be convenient, adjust budgets, advances and prices for 2026, and avoid changing the economic activity only to seek a lower rate if it does not correspond to the business reality.

The images of two advances filed for the January-February 2026 bimonthly period show the 30 per thousand rate for activity 5611, restaurant services, and activity 7020, consulting services, which are among the most affected by this increase.

Through Press Release 074 of May 19, 2026, the DIAN clarified that the increase in Bogotá’s consolidated ICA component does not mean that the national rates of the Simple Taxation Regime increased.

What happened is that Bogotá, through District Agreement 1019 of 2025, increased the consolidated ICA component rate for some SIMPLE taxpayers, especially those in group 3 and group 3 SIC, from 10 per thousand to 30 per thousand. These groups mainly include the sale of food and beverages, transportation, professional services, consulting and scientific activities.

| So did SIMPLE increase? | Not necessarily. According to the DIAN, the general SIMPLE rate was not increased by the National Government. What changes is the internal distribution of the tax. |

|---|---|

| The SIMPLE regime is made up of several elements, including the national SIMPLE component administered by the DIAN and the territorial ICA component belonging to the municipality or district. When Bogotá’s ICA component increases, the portion corresponding to the national SIMPLE component decreases. Therefore, the DIAN indicated that the change does not increase the total value of the RST advance; it represents an internal redistribution among the components of the consolidated tax. | Practical example |

| Suppose a group 3 taxpayer in Bogotá has bimonthly income of $100,000,000 and a consolidated SIMPLE rate of 3.4%. | Concept |

Taxpayer’s bimonthly income | $100,000,000 | $100,000,000

SIMPLE regime group | Group 3 | Group 3

Consolidated SIMPLE rate in the example | 3.40% | 3.40%

Total SIMPLE tax | $3,400,000 | $3,400,000

Bogotá ICA rate | 10 per thousand | 30 per thousand

Bogotá ICA component | $1,000,000 | $3,000,000

National DIAN component | $2,400,000 | $400,000

Total payable on the SIMPLE receipt | $3,400,000 | $3,400,000

Conclusion

The increase in SIMPLE ICA in Bogotá for 2026 is real, but it does not apply equally to everyone. The rates are 12, 16 or 30 per thousand, depending on the activity group.

The greatest impact will fall on taxpayers providing professional services, consulting, restaurants, food establishments and transportation, which are subject to the 30 per thousand rate.

It cannot be said that the SIMPLE tax in general increased. The correct statement is that, in Bogotá, the consolidated ICA component increased for certain groups within the SIMPLE regime.

Consequently, the general SIMPLE rate remains the same, but the distribution of the payment changes: Bogotá receives a larger share through ICA and the DIAN receives a smaller share through the national component.

For some taxpayers who already filed the SIMPLE advance for the January-February 2026 bimonthly period, this increase was not reflected.

If you have comments, contact us.

If this information helped you, leave us your comments here.

We provide tax advisory services.

Contact us; the first consultation is free: Tel / WhatsApp 310 558 91 17 – 313 821 48 03

Income tax return calendar for individuals, taxable year 2025

| Before the Bogotá ICA increase | After the Bogotá ICA increase | If you are required to file your income tax return for taxable year 2025, which is filed in 2026 according to the last two digits of your NIT or citizenship ID number, the maximum dates for filing the corresponding return apply. Remember that preparing the return takes time and must be done carefully, without rushing. It is recommended to begin the process now with your accountant and have it ready at least three days before the deadline. |

|---|---|---|

| Individuals not required to file an income tax return in 2026 for taxable year 2025. | All individuals and estates that meet all of the following conditions are not required to file an income tax return for taxable year 2025: | Condition |

| Limit or requirement | Not being responsible for VAT | Qualitative requirement |

| Gross assets at the end of the taxable year | Up to 4,500 UVT ($224,096,000) | Gross income |

| Less than 1,400 UVT ($69,719,000) | Credit card consumption | Up to 1,400 UVT ($69,719,000) |

| Total purchases and consumption | Up to 1,400 UVT ($69,719,000) | Bank deposits, deposits or financial investments |

| Up to 1,400 UVT ($69,719,000) | Minimum late-filing penalty | $524,000 |

| If you do not meet any of the above conditions, you must file the income tax return for 2025. | Documents required to prepare the income tax return for taxable year 2025 include, among others, the updated RUT certificate, income tax returns from the last two taxable years, documents supporting assets, income and deductions, bank statements, investment certificates, property and vehicle information, employment income and withholding certificates, certificates for dividends, fees, financial returns, donations, health payments, housing loan interest, expense invoices and payments made to employees. | Contact us and we will prepare your return. |

| Phone: 310 558 91 17 - 313 821 48 03 | Income Tax Return Advisory | Our income tax return advisory service, including the requirements for 2025-2026, allows us to identify the tax and fiscal obligations that apply and that, if unknown, may lead to non-compliance with formal and substantive obligations. Formal obligations refer to the duties that must be fulfilled in order to comply with substantive obligations. Examples of formal obligations include registration in the RUT, registration in the Tax Information Registry (RIT), and similar duties. Substantive obligations include, for example, filing income tax, VAT, ICA and other returns. |

These returns have minimum requirements to ensure their effectiveness, that is, to be considered properly filed. Otherwise, the return may be deemed ineffective, generating penalties and interest, which in many cases may be higher than the tax itself.

Proper advisory support can help you avoid excessive tax payments, penalties and interest.

For 2026, the DIAN minimum penalty is 10 UVT, that is, $524,000. For example, a return with $10,000 of tax payable, if not filed correctly, may turn into an amount payable greater than $524,000. The filing deadlines under the DIAN 2026 tax calendar must be taken into account.

Request advice with no obligation here, schedule an advisory appointment here, call 310 558 91 17, or check whether you must file an income tax return here.

Withholding Tax

Can withholding tax be filed without payment?

If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step.

Schedule an appointmentGeneral contact.

Prestamos asesoría en materia tributaria.

Contáctenos, la primera es gratis: Tel WA 310 558 91 17 – 313 821 48 03

Calendario de declaración de renta para personas naturales, año gravable 2025

Si está obligado a presentar su declaración de Renta por el año gravable 2025 que se presenta en 2026 de acuerdo con los dos últimos dígitos de su NIT o Cédula de ciudadanía, las siguientes son las fechas máximas para presentar la respectiva declaración. Pero recuerde, que el proceso de elaboración toma tiempo y se debe elaborar con especial cuidado, sin afanes, por lo que se recomienda iniciar el proceso desde ya en coordinación con su Contador y tenerla lista por lo menos tres días antes de la fecha de vencimiento.

Quiénes deben presentar declaración de renta del año 2025 a partir del 12 de agosto de 2026

NO obligados a declarar renta en 2026 por el año gravable 2025

Todas las personas naturales y sucesiones ilíquidas que cumplan las siguientes condiciones, NO deben presentar declaración de renta por el año gravable 2025:

Para no estar obligado a declarar renta por el año gravable 2025 deben cumplirse todas estas condiciones:

| Condición | Tope o requisito |

|---|---|

| No ser responsable del impuesto a las ventas IVA | Requisito cualitativo |

| Patrimonio bruto al cierre del año gravable | Hasta 4.500 UVT ($224.096.000) |

| Ingresos brutos | Inferiores a 1.400 UVT ($69.719.000) |

| Consumos con tarjeta de crédito | Hasta 1.400 UVT ($69.719.000) |

| Compras y consumos totales | Hasta 1.400 UVT ($69.719.000) |

| Consignaciones, depósitos o inversiones financieras | Hasta 1.400 UVT ($69.719.000) |

| Sanción mínima por extemporaneidad | $524.000 |

Si no cumple alguna de las anteriores condiciones, debe presentar declaración de renta del año 2025.

Documentos Necesarios para Elabora la Declaración de Renta Año Gravable 2025.

En coordinación con su Contador, deberá aportar los siguientes documentos entre otros como base para elaborar la declaración de renta.

Copia del certificado de inscripción en el Registro Único Tributario –RUT– debidamente actualizado.

Declaración de renta de los 2 últimos años gravables.

Documentos para determinar el patrimonio

Certificados o extractos de los saldos de las cuentas de ahorro y corrientes emitidos por las entidades financieras.

Certificados de las inversiones emitidos por las entidades donde se constituyó la inversión, por ejemplo: CDT, bonos, derechos fiduciarios, inversiones obligatorias, entre otras.

Declaración o estado de cuenta del impuesto predial de los bienes inmuebles que posea.

Escrituras de adquisición de los bienes inmuebles y/o certificados de instrumentos públicos.

Factura de compra o documento donde conste el valor de adquisición de los vehículos y estado de cuenta del impuesto de vehículos.

Relación de los muebles, enseres, máquinaria y equipo, por su valor de adquisición más adiciones y mejoras.

Certificado de avalúo técnico de los bienes incorporales tales como good will, derechos de autor, propiedad industrial, literaria, artística, científica y otros.

Letras, pagarés y demás documentos que respalden cuentas por cobrar y obligaciones o deudas, conforme a los requisitos de ley.

Documentos para determinar los ingresos

Certificado de ingresos y retenciones laborales.

Certificado de indemnizaciones por accidentes de trabajo o de enfermedad, maternidad, gastos de entierro del trabajador, seguro por muerte y compensaciones por muerte de miembros de las Fuerzas Militares y Policía Nacional.

Certificados por concepto de dividendos y participaciones recibidos en el año.

Certificados de indemnizaciones sustitutivas de la pensión o devoluciones de saldos de ahorro pensional.

Certificados de ingresos por concepto de honorarios, comisiones y servicios.

Certificados de rendimientos financieros pagados durante el año, expedidos por las entidades correspondientes.

Certificado de dividendos y participaciones recibidos durante el año, expedidos por las sociedades de las cuales es socio o accionista.

Certificados de ingresos recibidos durante el año por concepto de utilidades repartidas por sociedades liquidadas.

Certificados de pagos por concepto de alimentación, efectuados por su empleador.

Certificados de pago de indemnizaciones por seguros de vida.

Documentos para determinar los pagos que constituyen deducciones

Certificado de pagos de intereses por préstamos para adquisición de vivienda.

Certificados por pagos de salud obligatoria y medicina prepagada.

Certificados por inversiones en nuevas plantaciones de riegos, pozos, silos, centros de reclusión, en mantenimiento y conservación de obras audiovisuales, en librerías, proyectos cinematográficos y otros.

Certificados por donaciones a la Nación, departamentos, municipios, distritos, territorios indígenas y otros.

Relación de facturas de gastos, indicando el valor total.

Relación de los pagos efectuados a sus empleados por concepto de sueldos, bonificaciones, vacaciones, cesantías y otros.

Consultenos y elaboraremos su declaración.

Tel 310 558 91 17 - 313 821 48 03

Asesoría en Declaración de Renta

Nuestra asesoría en declaración de renta. (Consulte aquí los requisitos para el año 2025-2026) permite la identificación de las obligaciones que se tienen de tipo tributario y fiscal que al no conocerlas, trae como consecuencia el incumplimiento de obligaciones formales y sustanciales. Las primeras se refieren a los deberes que se debe atender con el fin de cumplir con las segundas, es decir con las sustanciales. Son ejemplo de obligaciones formales la inscripción en el RUT, Registro de Información Tributaria RIT, etc. Las obligaciones sustanciales son por ejemplo las declaración de Renta, IVA, ICA, etc.

Estas declaraciones tienen unos requisitos mínimos para asegurar su eficacia, es decir, que se den por presentadas correctamente, de lo contrario se puede incurrir en ineficacia de las mismas con la consecuente generación de sanciones e intereses, que en muchos casos es mayor que el mismo impuesto generado.

Una adecuada asesoría le puede evitar un pago excesivo por impuestos, así como de sanciones e intereses.

Para 2026 la sanción mínima de la DIAN es de 10 UVTs, es decir $524.000. Así por ejemplo una declaración con impuesto a pagar de $10.000 si no se presenta en debida forma puede convertirse en un valor por pagar superior a $524.000. Para lo anterior se debe tener en cuenta las fechas límites según el Calendario DIAN 2026 para el año 2026 de la DIAN.

Pida una asesoria sin compromiso Aquí ó Programe una cita de asesoría Aquí Tel 310 558 91 17 o verifique si debe Declarar Renta Aquí

- Details

- Category: Tax advisory

- Hits: 63

Accounting Bogotá

Value Added Tax (VAT) Advisory

Advisory services on Value Added Tax (VAT) for people who start a business activity or provide services and, when registering in the RUT, seek to be classified as not responsible for VAT (formerly the Simplified Regime), in order not to become responsible for Value Added Tax. However, even if they meet the legal requirements, doing so may cause them to lose many business opportunities because of the limitations this regime imposes.

Value Added Tax (VAT) Advisory

First, business growth and development are being limited. The purpose of starting a business is to achieve the fastest possible growth. However, although being classified as not responsible for VAT under obligation 49 in the RUT reduces obligations, it also significantly limits proper business development.

If you register under obligation 49 — Not responsible for VAT — you are setting limits on growth and development. By contrast, being classified under responsibility 48 — Sales Tax — not only considerably expands the field of action in business and avoids limiting growth out of fear of being reclassified, but the amounts payable as VAT may be minimal compared with the business development that can be achieved. For this, it is enough to comply with the filing deadlines according to the DIAN tax calendar for 2022.

The obligation to invoice is independent of VAT responsibility; therefore, a person may not be responsible for VAT and at the same time may be required to issue invoices. This is established by Unified Electronic Invoice Concept 100202208-106-RAD-91142 of August 19, 2022.

The first advisory session is FREE.

310 558 91 17 - 313 821 48 03

Would you like to pay less income tax to the DIAN and less Industry, Commerce and Signage Tax (ICA)?

For 2022, 2023 and subsequent years, the rate used to calculate tax in income tax returns for both individuals and legal entities in Colombia is 35%. In addition, ICA tax must be paid on the income received, and the rate depends on each municipality. These taxes represent a very high tax burden, especially for small companies and merchants, as well as for some professionals who work independently.

By registering under the Simple Taxation Regime (RST), the burden of complying with tax obligations is not only simplified; most importantly, the amount payable as taxes may be significantly reduced because the rates are much lower. RST rates range from 1.8% to 14.5%, and their application depends on gross income and the business activity carried out.

Contact us and we will help you evaluate the possibility of reducing your tax payments.

Remember: the first consultation is FREE. Request it here.If you need more information, advice or guidance, request an appointment here or write to

310 558 91 17 – 313 821 48 03Supporting Document for purchases made from parties not required to issue invoices

Do you know whether you must generate a Supporting Document for purchases made from parties not required to issue invoices?

According to DIAN Resolution 167 of December 30, 2021, the required parties had a deadline to implement it beginning May 2, 2022. However, through Resolution 488 of April 29, 2022, the DIAN postponed this obligation to August 1, 2022. Nevertheless, as with Electronic Invoicing and Electronic Payroll, this Supporting Document is already a reality, so implementation is necessary.

But who is required to do it?

You are required to generate it if you acquire goods or services from a supplier that is not required to issue a sales invoice, so that you can document the transaction and have support for costs, deductions or deductible taxes in your tax returns.

If you are an electronic invoicer, VAT-liable party, income tax and complementary tax taxpayer, and you need to support costs and deductions for income tax and complementary tax purposes, as well as deductible VAT, you must generate the Supporting Document.

Do you need more information? Request an appointment or contact us here or at:

310 558 91 17 - 313 821 48 03

Tax Value Unit (UVT) value, year 2026

Through Resolution 000238 of December 15, 2025, the DIAN set the value of the Tax Value Unit (UVT) applicable in 2026.

Concept | 2026 Value

Tax Value Unit (UVT) | $52,374

Minimum penalty | $524,000

| These values are used for different calculations in the assessment of taxes and penalties for omission or late filing. | As a business owner, you should focus your efforts on developing your company’s operations. We take care of the accounting, financial information, correct tax calculation and timely filing of taxes so that you do not incur unnecessary penalties. |

|---|---|

| Remember that we treat your accounting matter, situation or problem as our own in order to solve it quickly. | Contact us: +57 310 558 91 17 – 313 821 48 03 |

| Schedule your appointment for more personalized advice here. | New ICA rates in Bogotá as of 2022 |

With the issuance of District Agreement 780 of November 6, 2020, new rates were created for the Industry and Commerce Tax (ICA) in the city of Bogotá.

Article 6 of the Agreement modifies the Industry and Commerce Tax rate starting in taxable year 2022 for industrial, service and financial activities. Among others, professional consulting activities and services provided by contractors, builders and developers increased from 6.9 to 8.66 per thousand, while consulting services in the practice of a liberal profession decreased from 9.66 to 7.66 per thousand as of 2022.

Likewise, Article 5 establishes a temporary increase in ICA rates for taxable year 2021 for those who increased their income during the epidemiological situation caused by Coronavirus (COVID-19).

Later, Resolution No. SDH-000265 of April 13, 2021 adopted and updated the classification of economic activities (CIIU) and defined the ICA rates for all taxable activities in Bogotá.

For the correct application of Bogotá’s Industry and Commerce Tax, the District Treasury Secretariat has published the ICA Guide, which helps clarify questions when applying the tax.

These rates are important in order to apply the correct rate in ICA withholding processes. Learn here who the withholding agents are for Bogotá’s Industry and Commerce Tax and how the system operates.

According to the dynamics of ICA withholding under Resolution DDI-000305 of January 16, 2020 on withholding agents, Bogotá’s ICA Large Taxpayers are subject to withholding only by public entities and by large taxpayers designated by the DIAN. For 2026, Resolution DDI 029334 of October 31, 2025 designated Bogotá’s ICA Large Taxpayers.

The withholding system is governed, as applicable to the nature of the Industry and Commerce Tax, by the specific rules adopted by the Capital District and the general withholding rules applicable to income tax and complementary taxes.

To ensure efficient collection of the Industry and Commerce Tax, the Bogotá District Tax Directorate issued Resolution DDI-000305 of January 16, 2020, designating withholding agents for the Industry and Commerce Tax.

The following are withholding agents: public law entities; those classified as large taxpayers by the DIAN; those designated by the district tax director; intermediaries or third parties involved in transactions where ICA withholding is generated; consortiums and temporary unions when they make payments or credits to account to taxpayers under the ordinary or preferential ICA regime; and ordinary ICA regime taxpayers when the beneficiary is a taxpayer under the preferential regime and carries out taxed activities in the Capital District.

Withholding is not applied to payments or credits to non-ICA taxpayers, non-taxed or exempt payments, payments to public law entities, payments to a large taxpayer that files ICA in Bogotá except when the withholding agent is a public entity, resources from the health system capitation payment unit, public utility payments, or when a special taxable base applies, in which case withholding is applied on that base.

The ICA withholding rate is the rate corresponding to the respective activity. When the party subject to withholding does not report the activity or it cannot be established, the withholding rate is the maximum rate in force for the taxable period, and the transaction is taxed at that same rate.

Minimum bases to apply withholding for 2026:

Minimum withholding bases for 2026 (UVT value: $52,374)

Concept | Base in UVT | Base in pesos

Services | 4 UVT | $209,496

Purchases | 27 UVT | $1,414,098

Source: Bogotá District Treasury Secretariat - ICA.

If this information helped you, leave us your comments here.

We provide tax advisory services.

Contact us; the first consultation is free: Tel / WhatsApp 310 558 91 17 – 313 821 48 03

Expiration of DIAN electronic signature

The Electronic Signature replaced what was formerly called the Digital Signature. This mechanism is used by the DIAN to validate the information submitted by taxpayers. In this way, the tax authority ensures that the documents are generated directly by the responsible parties, that there is no impersonation, and therefore that the information has full legality and effectiveness. This mechanism was implemented in 2016.

Because this mechanism is valid for three years, it is possible that for some taxpayers it has already expired or is close to expiring. They may then have problems signing documents for submission to the DIAN and may incur late filing of tax obligations.

If it has not yet expired, the update procedure is very simple and can be completed online through the DIAN guide. If it has already expired, the process is somewhat more complex and may require an appointment with the DIAN.

If you need help or guidance, we will gladly assist you.

Contact us by email here or by phone at 313 821 48 03 – 310 558 91 17. The first consultation is FREE.

The DIAN requires independent professionals, salaried employees and restaurants

Within the “Up to Date with the DIAN” program, the DIAN carries out visits and other procedures for independent professionals, salaried employees and restaurants in order to encourage compliance with their obligations.

The tax authority estimates that many people, especially independent workers, do not comply with their tax obligations and may therefore be considered non-filers or evaders.

The DIAN currently has sufficient mechanisms to identify taxpayers who fail to comply with their obligations and who may be required to respond at any time.

When the DIAN issues a request, it is usually because it has sufficient information about the taxpayer. The best response is to pay proper attention to the request and become up to date with the DIAN. Possible penalties can often be much higher than the taxes themselves.

If you believe you have pending matters with the DIAN, it is better to act in time. Contact us and we will guide you through these procedures. Phone: 310 558 91 17. The first consultation is free.

https://www.dian.gov.co/descargas/EscritosComunicados/2017/170_Comunicado_de_prensa_27102017.pdf

| Restaurants, cafés, fruit shops, bakeries, fast-food outlets, bars, taverns and nightclubs have a defined regime for value added tax. These activities are generally not required to charge VAT, except in specific cases, but are subject to the National Consumption Tax (INC). | The simplified and ordinary INC regimes also apply to them. In both cases, those carrying out these activities have obligations, and non-compliance leads to penalties. Many of these businesses fail to comply with minimum legal operating requirements and are exposed to possible fines or penalties. By formalizing your business, you gain an advantage over others because you can focus on growth without fear. Proper classification under the correct regime ensures normal development of activities without creating additional burden. | With our advice, we identify whether you fall under the ordinary or simplified INC regime, clearly explaining the advantages and disadvantages in each case and proposing viable alternatives. We always seek compliance with tax regulations while also reducing costs to the maximum extent legally permitted. |

|---|---|---|

| Determine National and Local Tax Obligations | Carrying out a business activity or providing income-generating services implies national and local tax responsibilities. It is important to identify the obligations that apply in order to avoid possible investigations, penalties and late-payment interest costs. Acquiring these tax responsibilities does not necessarily mean that taxes will be payable. Identifying in time which responsibilities arise from carrying out business activities is essential to reduce unbudgeted and unexpected costs. | A request from a tax authority such as the DIAN or a municipal or local tax office can be exhausting, frustrating, costly, and may even seriously affect your personal assets. In many cases, several years may pass without any type of request. Tax authorities may let time pass, sometimes deliberately, and act during the final period legally available to them in order to secure higher revenue. These entities usually have up to five years to begin a process that may end in collection for all years that were not declared. |

| VAT, invoicing and Supporting Document | National Consumption Tax (INC). | Electronic Invoicing Advisory. |

Expiration of the DIAN electronic invoicing digital certificate.Can invoicing continue through a POS system?.

Supporting Document for purchases made from parties not required to issue invoices.If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step..

Schedule an appointment

General contact

Vencimiento de firma electrónica DIAN

Vencimiento de Firma Electrónica DIAN.

La Firma Electrónica reemplazó lo que antes se llamaba Firma Digital. Este mecanismo es utilizado por la DIAN para validar la información que los contribuyentes envían. De esta manera, la Entidad Fiscalizadora se asegura que son generados directamente por los responsables y que no hay suplantación, y en consecuencia tiene plena legalidad y eficacia. Este mecanismo se implementó a partir de 2016.

Como este mecanismo tiene una vigencia de tres (3) años, es muy posible que para algunos contribuyentes que la hayan tramitado, ya este vencida o este próxima a hacerlo, y por lo tanto, puedan presentar problemas al momento de firmar los documentos para envío a la DIAN, y caer en una eventual extemporaneidad en la presentación de las Obligaciones tributarias como la Retención en la Fuente de acuerdo a las fechas del Calendario Tributario 2020 y sus modificaciones realizadas a casusa del Estado de Emergencia que invocó el Gobierno Nacional a raíz de situación mundial con respecto a COVID-19

Solución

Si aún no se ha vencido, el procediendo de actualización es muy sencillo y se hace vía WEB (ver paso a paso) https://www.dian.gov.co/impuestos/Firma%20Electrnica/1pasoapaso.pdf, sin embargo, si el vencimiento ya se produjo, el proceso es un poco más complejo y más aun teniendo en cuenta las restricciones de movilidad, ya que este trámite se requiere hacer de forma presencial, no obstante, este servicio por ahora se puede hacer vía WEB mediante solicitud de cita en la DIAN desde https://agendamientodigiturno.dian.gov.co/ y seguir el proceso el cual puede durar algunos días.

Si requiere ayuda u orientación con gusto le podemos colaborar.

Consúltenos mediante correo electrónico AQUI o a los teléfonos Cels 313 821 48 03 – 310 558 91 17. La primera consulta es GRATIS.

DIAN requiere a independientes, asalariados y restaurantes

La DIAN dentro del programa "Al dia con la DIAN" adelanta visistas y otras diligencias a Profesionales Independientes, Asalariados y Restaurantes con el animo de procurar el cumplimiento de las obligaciones de estas personas.

La entidad fiscalizadora estima que son muchas las personas, especialemente independientes que no cumplen las obligaciones tributarias por lo cual pueden ser considerados como omisos o evasores.

Se debe recordar que en la actualidad la DIAN cuenta con los mecanismos suficientes para identificar a los contribuyentes que no cumplen con sus obligaciones y que en cualquier momento seran requeridos.

Con frecuencia, cuando la DIAN efectua un requerimiento, es por que cuenta con la suficiente informacion del contribuyente, y lo mejor que puede hacer este contribuyente es prestarle la suficiente atencion al mismo y buscar la forma de ponerse " AL dia con la DIAN". pero no debe olvidar que puede incurrir en probables sanciones las cuales en muchas ocaciones son mucho mas elevadas que los mismos impuestos a pagar.

En concecuenia, si usted cree que tiene asuntos pendientes con la DIAN, es mejor actuar a tiempo. Contáctenos y lo orientamos en estos procedimientos. Tel 310 558 91 17. La primera consulta es gratis.

https://www.dian.gov.co/descargas/EscritosComunicados/2017/170_Comunicado_de_prensa_27102017.pdf

Impuesto Nacional al Consumo INC.

Los restaurantes, cafeterías, fruterías, panaderías, expendio de comidas rápidas, bares, tabernas, discotecas tienen un régimen definido en cuanto al valor agregado. Estas actividades no están en la obligación de cobrar el IVA, salvo excepciones, sino que están sometidas al Impuesto Nacional al Consumo INC.

También les aplica el Régimen Simplificado y el Común del INC. En ambos casos los ejecutores de estas actividades tienen unas obligaciones cuyo incumplimiento deriva en sanciones. Muchos de los negocios mencionados incumplen los mínimos lineamientos legales de funcionamiento por lo que están expuestos a eventuales multas o sanciones. Al formalizar su negocio tienen ventaja frente a los demás ya que se pueden concentrar en el crecimiento del mismo sin temor alguno. Una adecuada clasificación del régimen asegura un desarrollo normal de actividades sin que implique mayor desgaste.

Con nuestra asesoría se identifica si usted aplica al Régimen Común o Simplificado del Impuesto Nacional al Consumo INC indicándole de forma clara las ventajas y desventajas en cada caso proponiendo alternativas viables buscando siempre el cumplimento de la norma tributaria pero buscando también la reducción de los costos al máximo permitido en la búsqueda de un justo equilibrio

Determinar las Obligaciones Fiscales Nacionales y Locales

El hecho de desarrollar una actividad mercantil o de prestación de servicios generadora de renta, implica que se tienen unas responsabilidades de orden tributario nacional y local. Es importante identificar las obligaciones que se tienen con el objeto de evitar posibles investigaciones con las eventuales sanciones y costos por intereses de mora. Al adquirir estas responsabilidades fiscales, no implica que la consecuencia sea la de pagar impuestos. Identificar a tiempo qué responsabilidades se adquieren por desarrollar actividades mercantiles es fundamental para disminuir costos no presupuestados e inesperados.

El requerimiento de una entidad fiscalizadora como la DIAN o Oficina de impuestos municipales o locales puede ser desgastante, frustrante, oneroso e incluso puede comprometer seriamente su patrimonio personal. En muchos casos pueden pasar varios años sin que haya algún tipo de requerimiento. Las entidades fiscalizadoras pueden dejar pasar el tiempo a veces deliberadamente y actuar en los últimos momentos que legalmente les está permitido con el fin asegurar un mayor ingreso. Normalmente estas entidades tienen hasta cinco años para iniciar un proceso que puede terminar en cobros de todos los años dejados de declarar.