- Details

- Category: Tax advisory

- Hits: 50

Accounting Bogotá

Can invoicing continue through a POS system?

POS receipts, that is, those generated through a cash register or computer program, may no longer be issued when the purchase exceeds 5 UVT ($212,060 for 2023). This is provided in paragraph 2 of Article 13 of Law 2155 of September 14, 2021, which modifies Article 616-1 of the Tax Code. This means that for sales above that amount, an electronic invoice must necessarily be prepared, especially when the buyer needs to support the purchase as a cost or expense, since amounts invoiced on a POS receipt are not deductible.

Key information

This became effective as of February 1, 2023, according to the schedule established in Resolution 001092 of July 1, 2022.

Therefore, if you are required to issue invoices and had been doing so through a POS system, the most advisable course is to implement Electronic Invoicing if you have not already done so, because buyers will likely request an invoice. It should be noted that once the POS receipt is generated, it is not possible to request that it be replaced with an electronic invoice, and that cost or expense cannot be deducted. This is established in Unified Electronic Invoice Concept 100202208-106-RAD-911 of August 19, 2022, section 3.3.2.1.

Likewise, if you are an income tax taxpayer or are responsible for VAT and need the cost or expense of goods or services acquired to be deductible in the income tax return, or if you want to deduct the VAT paid in the VAT return, those items must be supported by an electronic invoice and not by a POS receipt, regardless of the amount. For example, POS receipts for gasoline purchases are not deductible. Consequently, it is best to request an electronic invoice for all payments made.

If you are thinking about creating your own company, with the DIAN’s free solution you can begin as an electronic invoicer, comply with the rules and avoid possible penalties.

Contact us so that, through professional advice, you can carry out a successful process as an electronic invoicer.

Remember that the first consultation is FREE, or schedule a personalized appointment here.

310 558 91 17 - 313 821 48 03

- Details

- Category: Tax advisory

- Hits: 70

Accounting Bogotá

Expiration of the DIAN electronic invoicing digital certificate

For many individuals and legal entities required to issue electronic invoices, and who began as electronic invoicers in 2020 using the DIAN’s free solution, the digital certificates that allow them to validate those documents before the DIAN have expired or are close to expiring. It should be remembered that digital certificates are valid for one year, and once they expire, invoices cannot be generated.

Key information

If this is your case, it is necessary to process the renewal of that certificate in order to continue invoicing.

Contact us here so we can provide the relevant advice at 310 558 91 17 or through /contacto#cb-contact-form and

- Details

- Category: Tax advisory

- Hits: 64

Accounting Bogotá

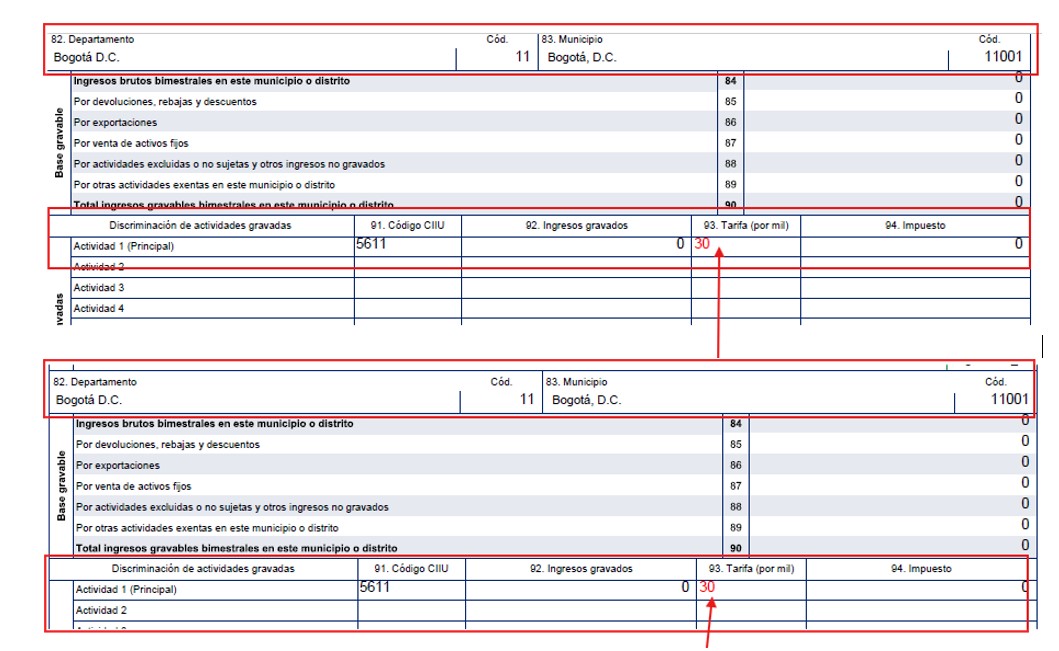

New ICA rates in Bogotá as of 2022

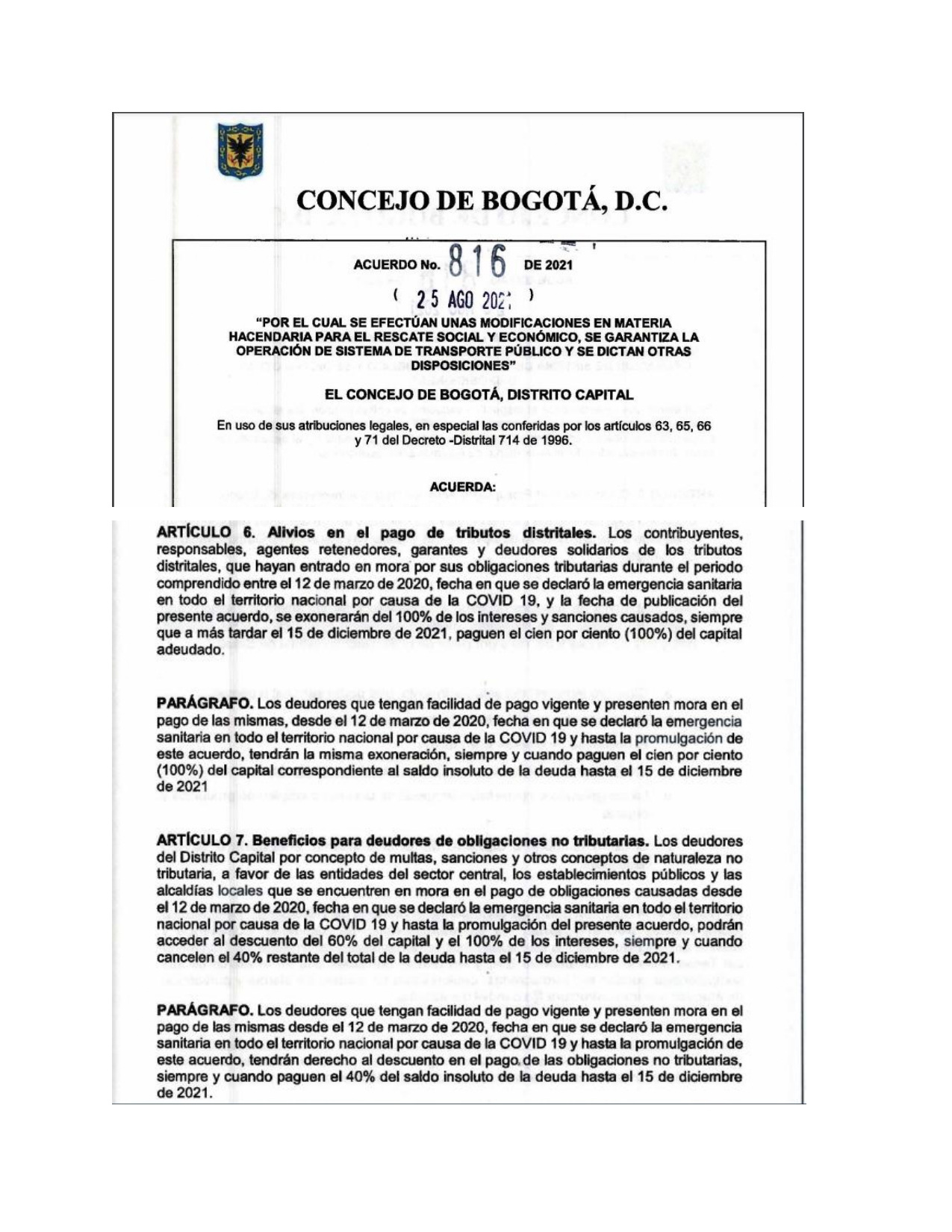

With the issuance of District Agreement 780 of November 6, 2020, new rates were created for the Industry and Commerce Tax (ICA) in the city of Bogotá.

Key information

Article 6 of the Agreement modifies the Industry and Commerce Tax rate, starting in taxable year 2022, for industrial, service and financial activities. Among others, professional consulting activities and services provided by contractors, builders and developers increased from 6.9 to 8.66 per thousand, while consulting services in the practice of a liberal profession decreased from 9.66 to 7.66 per thousand as of 2022.

Likewise, Article 5 establishes a temporary increase in ICA rates for taxable year 2021 for those who increased their income during the epidemiological situation caused by Coronavirus (COVID-19).

Later, Resolution No. SDH-000265 of April 13, 2021 adopted and updated the classification of economic activities (CIIU) and defined the ICA rates for all taxable activities in Bogotá.

It resolves:

ARTICLE 1. To establish the classification of economic activities for purposes of the administration, control, collection and determination of the Industry and Commerce Tax in the Capital District of Bogotá. See here the ICA activities and rates for 2022, 2023, 2024, 2025 and 2026.For the correct application of Bogotá’s Industry and Commerce Tax, the District Treasury Secretariat (SDH) has published the ICA Guide, which undoubtedly helps clarify several questions when applying the tax.

These rates are important in order to apply the correct rate in ICA withholding processes. Learn here who the withholding agents are for Bogotá’s Industry and Commerce Tax and how the system operates.

According to the dynamics of how ICA withholding operates among taxpayers under Article 2, “Operation of the System,” of Resolution DDI-000305 of January 16, 2020 on withholding agents, Bogotá’s ICA Large Taxpayers are subject to withholding only by public entities and by large taxpayers designated by the DIAN. For 2026, Resolution DDI 029334 of October 31, 2025 designated Bogotá’s ICA Large Taxpayers.The withholding system is governed, as applicable to the nature of the Industry and Commerce Tax, by the specific rules adopted by the Capital District and the general withholding system rules applicable to income tax and complementary taxes.

To ensure efficient collection of the Industry and Commerce Tax, the Bogotá District Tax Directorate issued Resolution DDI-000305 of January 16, 2020, designating withholding agents for the Industry and Commerce Tax.

The following are withholding agents:

Public law entities.

Those classified as large taxpayers by the DIAN.

Those designated as withholding agents by resolution of the district tax director.

Intermediaries or third parties that participate in economic operations in which ICA withholding is generated.

Consortiums and temporary unions when they make payments or credits to account to taxpayers under the ordinary and/or preferential ICA regime in taxed transactions within the Capital District.

Ordinary ICA regime taxpayers when the payment beneficiary belongs to the preferential regime and carries out taxed activities within the Capital District.

As of July 1, 2004, ordinary ICA regime taxpayers must also apply ICA withholding to beneficiaries registered under the ordinary regime if they are independent professionals and participate in taxed activities within Bogotá.

Circumstances under which withholding is NOT applied:

Payments or credits to account made to non-ICA taxpayers.

Payments or credits to account that are not subject to tax or are exempt.

When the beneficiary of the payment is a public law entity.

When the beneficiary is classified as a large taxpayer by the DIAN and is an ICA filer in Bogotá, except when the withholding agent is a public entity.

Resources from the capitation payment unit of the subsidized and contributory regimes of the General Social Security Health System.

Payments for public utilities.

If there is a special taxable base, withholding is applied on that base.

The ICA withholding rate is the rate corresponding to the respective activity. When the party subject to withholding does not report the activity or it cannot be established, the withholding rate is the maximum rate in force for the Industry and Commerce Tax within the taxable period, and the transaction is taxed at that same rate.

Minimum bases to apply withholding for 2026:

Minimum withholding bases for 2026 (UVT value: $52,374)

Concept | Base in UVT | Base in pesos

| Purchases | 27 UVT | $1,414,098 |

|---|---|---|

| Source: Bogotá District Treasury Secretariat - ICA. | If this information helped you, leave us your comments here. | We provide tax advisory services. |

| Contact us; the first consultation is free: Tel / WhatsApp 310 558 91 17 – 313 821 48 03 | If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step. | Schedule an appointment |

General contactSecretaría Distrital de Hacienda de Bogotá - ICA.

Si la anterior informacion les ayudó, déjenos sus comentarios aquí.

Prestamos asesoría en materia tributaria.

Contáctenos, la primera es gratis: Tel WA 310 558 91 17 – 313 821 48 03

- Details

- Category: Tax advisory

- Hits: 61

Accounting Bogotá

National Consumption Tax (INC)

Restaurants, cafés, fruit shops, bakeries, fast-food outlets, bars, taverns and nightclubs have a defined regime for value added tax. These activities are generally not required to charge VAT, except in specific cases, but are subject to the National Consumption Tax (INC).

Key information

The simplified and ordinary INC regimes also apply to them. In both cases, those carrying out these activities have obligations, and non-compliance leads to penalties. Many of these businesses fail to comply with minimum legal operating requirements and are exposed to possible fines or penalties. By formalizing your business, you gain an advantage over others because you can focus on growth without fear. Proper classification under the correct regime ensures normal development of activities without creating additional burden.

With our advice, we identify whether you fall under the ordinary or simplified regime of the National Consumption Tax (INC), clearly explaining the advantages and disadvantages in each case and proposing viable alternatives. We always seek compliance with tax regulations while also reducing costs to the maximum extent legally permitted in pursuit of a fair balance.