- Details

- Category: Labor and payroll advisory

- Hits: 47

Accounting Bogotá

Electronic Payroll

New schedule to implement Electronic Payroll.

Key information

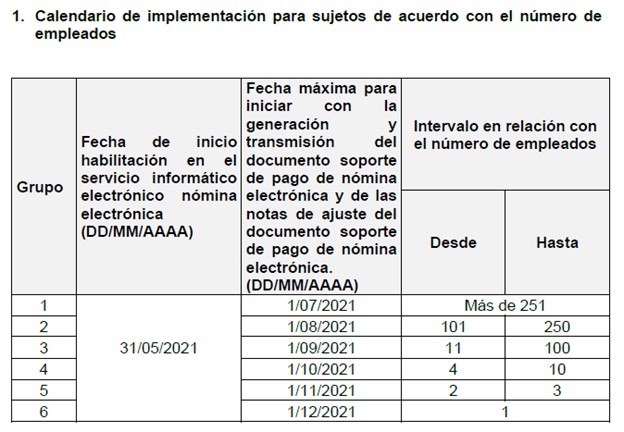

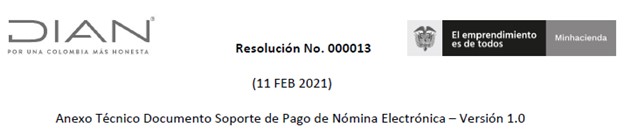

Through Resolution 037 of May 5, 2021, the DIAN modified Article 6, paragraphs 1 and 2, of Resolution 000013 of February 11, 2021, establishing new deadlines to begin the Electronic Payroll authorization process.

It should be noted that parties required to send Electronic Payroll reports to the DIAN and belonging to group 4, that is, with 1 to 10 employees, have an additional deadline in 2022 for transmission. Check it here.

The general schedule is as follows:

Through Resolution 13 of February 11, 2021, “whereby the electronic invoicing system implements and develops the functionality of the electronic payroll payment supporting document and adopts the technical annex for this document,” the National Government, through the DIAN, imposes another obligation on companies, whether individuals or legal entities. They must implement the Electronic Payroll process starting May 31, 2021, taking into account the implementation schedule based on the number of employees.

Although this process, as happened with Electronic Invoicing, may undergo changes in its schedule, it is already a reality. Individuals and legal entities required to implement it must begin doing so now.

Because the experience with Electronic Invoicing may make the process easier, since it operates similarly, it is necessary to make adjustments to payroll processes for a successful transition. As with Electronic Invoicing, the participation of several actors is also required, as are technological requirements such as a digital signature and an in-house or external technology provider.

It is very likely that the DIAN will also need to provide this mechanism for small companies so that it does not become too costly for them.

At www.contabilidadbogota.com, we offer advisory services for the implementation of Electronic Payroll and for determining whether you are required to do so.

Contact us; the first consultation is free: 310 558 91 17 – 313 821 48 03

- Details

- Category: Labor and payroll advisory

- Hits: 61

Accounting Bogotá

New deadline for Electronic Payroll

There is more time to submit Electronic Payroll for employers with 1 to 10 employees.

Key information

The deadline for submitting Electronic Payroll has again been extended for employers with up to 10 employees on their payroll. This was established in DIAN Press Release 027 of March 2, 2022, based on Resolution No. 000028 of February 28, 2022. The release states that, in this case, employers must generate and transmit the first electronic payroll payment supporting document and the adjustment notes for that document as follows: the months of December 2021, January 2022 and February 2022, independently, within the first ten business days of May 2022; and the months of March, April and May 2022, independently, within the first ten business days of June 2022.

Despite the above, and even if this applies, required parties are advised not to continue postponing the process and to continue as if the deadlines had not been extended.

If you have between 1 and 10 employees, you must report payroll to the DIAN beginning with December 2021. However, there is relief for these small employers who, for different reasons, have not done so.

In Resolution 151 of December 10, the DIAN states in its considerations that companies must focus their efforts on developing their operations and that “it is necessary to establish a special deadline for complying with the generation and transmission of the electronic payroll payment supporting document for those required parties.” Therefore, it granted a deadline until the first 10 days of March 2022 to generate and transmit the payroll for December 2021, January 2022 and February 2022.

Accordingly, many employers with up to 10 employees have more time to comply with this obligation. It should be noted that if the employer has already implemented the system, this deadline does not apply and the employer must comply with the schedule established in Resolutions 37 of May 5 and 63 of July 30, 2021.

Likewise, according to unofficial versions, the DIAN is developing a free solution for this group of required parties. It is believed that it should be ready before March 2022 and that, as with the DIAN’s free Electronic Invoicing solution, employers would not need to hire services from external providers.

Remember that even if you have only one employee on payroll and are required to generate Electronic Payroll for the DIAN, you must transmit the payroll for December, January and February by March 10, 2022.

As a business owner, you should focus your efforts on developing your company’s operations. We take care of the payroll implementation process.

We treat your accounting matter, situation or problem as our own in order to solve it quickly.

If you need more information or need help with implementation, contact us here. The first consultation is FREE.

310 558 91 17 - 313 821 48 03

If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step.

- Details

- Category: Labor and payroll advisory

- Hits: 53

Accounting Bogotá

Do you know whether you are required to generate Electronic Payroll?

Not everyone is required to generate and transmit electronic payroll for their employees.

Key information

According to DIAN Resolution 013, every taxpayer that hires staff or has payroll through an employment contract is required to generate and transmit payroll to the DIAN within the established deadlines.

Article 4 identifies the parties required to generate and transmit the payroll payment supporting document and adjustment notes. This responsibility lies with income tax and complementary tax taxpayers who want to include those costs or expenses as deductions in income tax returns and as deductible taxes in VAT returns. Therefore, if you have employees but do not file an income tax return, you are not required to generate Electronic Payroll.

It should be noted that parties required to send Electronic Payroll reports to the DIAN with up to 10 employees have a new deadline for transmission. Check it here.

As a business owner, you should focus your efforts on developing your company’s operations. We take care of the payroll implementation process.

We treat your accounting matter, situation or problem as our own in order to solve it quickly.

If you need more information or need help with implementation, contact us.

310 558 91 17 - 313 821 48 03

- Details

- Category: Labor and payroll advisory

- Hits: 64

Accounting Bogotá

How much does it cost to have an employee in Colombia earning the minimum wage?

The minimum wage in Colombia for 2026.

Key information

With the issuance of Decree 0159 of February 19, 2026, the amount of the minimum wage for 2026 was defined at $1,750,905. This means that for an employee who works full time, between 6 and 8 hours per day and 44 hours per week, the minimum amount payable for services is $1,750,905 plus all other factors that make up salary under the Substantive Labor Code. Assuming the employee works only daytime daily hours and no holidays, the employer’s monthly cost is $2,765,488, broken down as follows:

| Concept | Monthly value |

|---|---|

| Salary | $1,750,905 |

| Transportation allowance | $249,095 |

| Service bonus | $166,600 |

| Severance pay | $166,600 |

| Interest on severance pay | $19,992 |

| Vacation | $73,012 |

| Health contributions | $0 |

| Pension contributions | $210,108 |

| ARL occupational risk rate I | $9,140 |

| SENA exempt under Article 114-1 (1) | $0 |

| ICBF exempt under Article 114-1 (1) | $0 |

| Compensation fund | $70,036 |

| Estimated work clothing/equipment (2) | $50,000 |

| Total monthly cost | $2,765,488 |

(1) Article 114-1. Exemption from contributions. Companies, legal entities and similar entities that are income tax and complementary tax filers are exempt from paying payroll contributions to the National Learning Service (SENA), the Colombian Family Welfare Institute (ICBF), and contributions to the contributory health regime for workers who individually earn less than ten (10) current legal monthly minimum wages.

Likewise, individual employers are exempt from paying payroll contributions to SENA, ICBF and the health social security system for employees earning less than ten (10) current legal monthly minimum wages. This does not apply to individuals who employ fewer than two workers, who remain required to make the contributions referred to in that paragraph.

(2) Article 230 and following of the Substantive Labor Code do not determine a specific amount for work clothing/equipment; they only state that one pair of shoes and one work outfit must be supplied every four months. Therefore, we estimate a minimum monthly value of $50,000.

This information is vital when deciding to hire one or more employees because it allows the true cost to be known in advance. Many times, at first glance, only the minimum wage is considered as the only monthly payroll cost, creating an imbalance in the income budget. This generally occurs among employers who do not keep proper accounting records, and more frequently among individual employers who do not keep accounting records and do not have proper labor advice.

As a business owner, you should focus your efforts on developing your company’s operations. We take care of labor advice and the correct calculation of your payroll.

Remember that we treat your accounting matter, situation or problem as our own in order to solve it quickly.

310 558 91 17 - 313 821 48 03