- Details

- Category: Resources

- Hits: 64

Accounting Bogotá

Single Registry of Beneficial Owners (RUB)

Within the framework of the fight against corruption, money laundering, terrorism financing and tax evasion, the National Government, through Article 16 of Law 2155 of September 14, 2021, modified Article 631-5 of the Tax Code, defining the concept of Beneficial Owner. Article 17 created the Single Registry of Beneficial Owners (RUB) as part of the Single Tax Registry (RUT). Through this registry, all entities with a RUT and Non-Legal-Entity Structures (SIESPJ) and similar structures not required to register in the RUT must provide information about the beneficial owners of those entities.

Key information

A beneficial owner is defined as “the natural person or persons who ultimately own or control, directly or indirectly, a client and/or the natural person on whose behalf a transaction is carried out. It also includes the natural person or persons who exercise effective and/or final control, directly or indirectly, over a legal entity or another structure without legal personality.”

A) The following are beneficial owners of a legal entity:

1. The natural person who, acting individually or jointly, directly or indirectly owns five percent (5%) or more of the capital or voting rights of the legal entity, and/or benefits from five percent (5%) or more of the assets, returns or profits of the legal entity; and

2. The natural person who, acting individually or jointly, exercises control over the legal entity by any means other than those established in the previous paragraph; or

3. When no natural person is identified under the two previous paragraphs, the natural person who holds the position of legal representative must be identified, unless there is another natural person with greater authority in relation to the management or direction functions of the legal entity.

B) The following natural persons are beneficial owners of a structure without legal personality or a similar structure:

1. Settlor, trustor, founder or similar or equivalent position;

2. Trustee or similar or equivalent position;

3. Trust committee, financial committee or similar or equivalent position;

4. Beneficiary or conditional beneficiary; and

5. Any other natural person who exercises effective and/or final control, or who has the right to enjoy and/or dispose of the assets, benefits, results or profits.

Parties required to file the RUB and deadlines:

Resolution 164 of December 27, 2021 regulated Articles 631-5 and 631-6 of the Tax Code and adopted the technical annex to that Resolution, defining the characteristics and content of the file through which Beneficial Owners are reported.

Law 2195 of January 18, 2022 adopted measures on transparency, prevention and the fight against corruption. It establishes administrative and sanctioning liability against legal entities and branches of foreign companies for acts of corruption, as well as administrative sanctions and the grading of sanctions applicable to those persons. It also establishes the obligation to implement transparency and business ethics programs that include internal audit mechanisms and rules; establishes penalties for violations of prohibitions related to commercial books; and identifies the entities that have access to the Single Registry of Beneficial Owners (RUB).

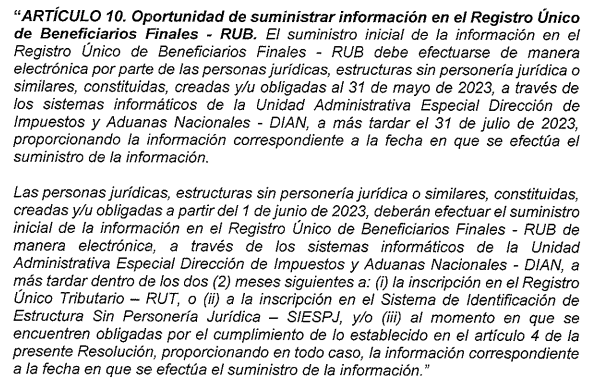

Article 4 of Resolution 164 of December 27, 2021 establishes the parties required to provide information in the RUB; Article 8 defines the content of the information to be provided; and Article 10 established the schedule for sending the requested information to the DIAN as follows: legal entities, structures without legal personality or similar structures created before January 15, 2022 had to submit the information no later than September 30, 2022. Legal entities, structures without legal personality or similar structures created on or after January 15, 2022 had to submit it no later than two months after registration in the RUT or SIESPJ.

Schedule modification:

Resolution 1240 of September 28, 2022 modified Articles 10 and 13 of Resolution 164 of December 27, 2021, that is, the calendar for providing this information. The schedule was as follows:

Legal entities, structures without legal personality or similar structures created before May 31, 2023 must provide the information no later than July 31, 2023.

Legal entities, structures without legal personality or similar structures created on or after June 1, 2023 must provide it no later than two months after registration in the RUT or SIESPJ.

| Creation date | Submission deadline |

|---|---|

| Before May 31, 2023 | Until July 31, 2023 |

| As of June 1, 2023 | Two months after creation |

For all of the above, this obligation should be addressed in a timely manner to avoid the penalties established in Article 20 of Resolution 164 of December 27, 2021, in accordance with Articles 631-6, 651 and 658-3 of the Tax Code.

Remember that to carry out this procedure, obligation 55 must first be included: Beneficial Owner Reporter — legal entity, structure without legal personality or similar structure required to report Beneficial Owners (Article 631-6 of the Tax Code).

For greater clarity on the subject, the DIAN made information available on:

Regulations for the Single Registry of Beneficial Owners (RUB).

Practical tools for the Single Registry of Beneficial Owners (RUB).

General information about the Single Registry of Beneficial Owners (RUB).

If this information helped you, remember to visit us and share your opinion.If you require our advice, contact us at:.

310 558 91 17 - 313 821 48 03

If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step.

- Details

- Category: Resources

- Hits: 66

Accounting Bogotá

Resources

Access consultation resources and tools.

- Details

- Category: Resources

- Hits: 61

Accounting Bogotá

Frequently Asked Questions

Within the framework of the fight against corruption, money laundering, terrorism financing and tax evasion, the National Government, through Article 16 of Law 2155 of September 14, 2021, modified Article 631-5 of the Tax Code, defining the concept of Beneficial Owner. Article 17 created the Single Registry of Beneficial Owners (RUB) as part of the Single Tax Registry (RUT). Through this registry, all entities with a RUT and Non-Legal-Entity Structures (SIESPJ) and similar structures not required to register in the RUT must provide information about their beneficial owners.

Single Registry of Beneficial Owners (RUB)

Within the framework of the fight against corruption, money laundering, terrorism financing and tax evasion, the National Government, through Article 16 of Law 2155 of September 14, 2021, modified Article 631-5 of the Tax Code, defining the concept of Beneficial Owner. Article 17 created the Single Registry of Beneficial Owners (RUB) as part of the Single Tax Registry (RUT). Through this registry, all entities with a RUT and Non-Legal-Entity Structures (SIESPJ) and similar structures not required to register in the RUT must provide information about the beneficial owners of those entities.

A beneficial owner is defined as “the natural person or persons who ultimately own or control, directly or indirectly, a client and/or the natural person on whose behalf a transaction is carried out. It also includes the natural person or persons who exercise effective and/or final control, directly or indirectly, over a legal entity or another structure without legal personality.”

A) The following are beneficial owners of a legal entity:

1. The natural person who, acting individually or jointly, directly or indirectly owns five percent (5%) or more of the capital or voting rights of the legal entity, and/or benefits from five percent (5%) or more of the assets, returns or profits of the legal entity; and

2. The natural person who, acting individually or jointly, exercises control over the legal entity by any means other than those established in the previous paragraph; or

3. When no natural person is identified under the two previous paragraphs, the natural person who holds the position of legal representative must be identified, unless there is another natural person with greater authority in relation to the management or direction functions of the legal entity.

B) The following natural persons are beneficial owners of a structure without legal personality or a similar structure:

1. Settlor, trustor, founder or similar or equivalent position;

2. Trustee or similar or equivalent position;

3. Trust committee, financial committee or similar or equivalent position;

4. Beneficiary or conditional beneficiary; and

5. Any other natural person who exercises effective and/or final control, or who has the right to enjoy and/or dispose of the assets, benefits, results or profits.

Parties required to file the RUB and deadlines:

Resolution 164 of December 27, 2021 regulated Articles 631-5 and 631-6 of the Tax Code and adopted the technical annex to that Resolution, defining the characteristics and content of the file through which Beneficial Owners are reported.

Law 2195 of January 18, 2022 adopted measures on transparency, prevention and the fight against corruption. It establishes administrative and sanctioning liability against legal entities and branches of foreign companies for acts of corruption, as well as administrative sanctions and the grading of sanctions applicable to those persons. It also establishes the obligation to implement transparency and business ethics programs that include internal audit mechanisms and rules; establishes penalties for violations of prohibitions related to commercial books; and identifies the entities that have access to the Single Registry of Beneficial Owners (RUB).

Article 4 of Resolution 164 of December 27, 2021 establishes the parties required to provide information in the RUB; Article 8 defines the content of the information to be provided; and Article 10 established the schedule for sending the requested information to the DIAN as follows: legal entities, structures without legal personality or similar structures created before January 15, 2022 had to submit the information no later than September 30, 2022. Legal entities, structures without legal personality or similar structures created on or after January 15, 2022 had to submit it no later than two months after registration in the RUT or SIESPJ.

Schedule modification:

Resolution 1240 of September 28, 2022 modified Articles 10 and 13 of Resolution 164 of December 27, 2021, that is, the calendar for providing this information. The schedule was as follows:

Legal entities, structures without legal personality or similar structures created before May 31, 2023 must provide the information no later than July 31, 2023.

Legal entities, structures without legal personality or similar structures created on or after June 1, 2023 must provide it no later than two months after registration in the RUT or SIESPJ.

| Creation date | Submission deadline |

|---|---|

| Before May 31, 2023 | Until July 31, 2023 |

| As of June 1, 2023 | Two months after creation |

For all of the above, this obligation should be addressed in a timely manner to avoid the penalties established in Article 20 of Resolution 164 of December 27, 2021, in accordance with Articles 631-6, 651 and 658-3 of the Tax Code.

Remember that to carry out this procedure, obligation 55 must first be included: Beneficial Owner Reporter — legal entity, structure without legal personality or similar structure required to report Beneficial Owners (Article 631-6 of the Tax Code).

For greater clarity on the subject, the DIAN made information available on:

Regulations for the Single Registry of Beneficial Owners (RUB).

Practical tools for the Single Registry of Beneficial Owners (RUB).

General information about the Single Registry of Beneficial Owners (RUB).

If this information helped you, remember to visit us and share your opinion.If you require our advice, contact us at:.

310 558 91 17 - 313 821 48 03

How to know whether I must file an income tax return

How do I know whether I must file an income tax return?

The dates are approaching for individuals to file their income tax returns for taxable year 2017. Many people wonder how to know whether they must file an income tax return and how to do so.

Decree 1950 of 2017 determines the filing dates for tax returns in 2018. This decree modifies the Single Tax Decree as follows:

“Article 1.6.1.13.2.15. Income tax and complementary tax return for individuals and estates. For taxable year 2017, individuals and estates must file the income tax and complementary tax return under the schedular system, using the form prescribed by the Special Administrative Unit of the National Tax and Customs Directorate (DIAN), except for those identified in Article 1.6.1.13.2.7 of this Decree, as well as assets destined for special purposes by virtue of donations and modal assignments whose donees or assignees do not personally enjoy them, and non-resident individuals who obtain income through permanent establishments in Colombia.”

Who did not have to file an income tax return for 2017:

Gross assets on the last day of taxable year 2017 did not exceed 4,500 UVT ($143,366,000).

Gross income was less than 1,400 UVT, that is, $44,603,000.

Credit card consumption did not exceed 1,400 UVT, $44,603,000.

Total purchases and consumption did not exceed 1,400 UVT, $44,603,000.

The total accumulated value of bank deposits, deposits or financial investments did not exceed 1,400 UVT, $44,603,000.

Nevertheless, to determine whether you are required to file an income tax return, it is important to carry out a personalized analysis, because each case is different.

It is very important to confirm whether or not you are required to file your return. Even if, at first glance, the general requirements above suggest that you are not required to file, there may be other circumstances you are unaware of that could include you among those required to file.

It should be remembered that filing an income tax return does not necessarily mean that tax must be paid. There are many returns where the amount payable is very low or even zero pesos, and many others produce a balance in favor. However, if you do not file when you are required to do so, in most cases it is more costly because the return must be filed with the corresponding late-filing penalty and late-payment interest.

There are less than two months before the deadlines begin. Individuals whose ID numbers end in 00 and 99 have until August 9.

Contact us; the first consultation is free.

How to cancel the RUT before the DIAN

There are many reasons why a taxpayer must request cancellation of the RUT before the DIAN. For example, when an SAS is closed, in addition to obtaining cancellation of the commercial registration at the Chamber of Commerce, cancellation of the RUT must be requested. This process can be completed virtually, and the corresponding video shows the step-by-step procedure.

If you require personalized advice, contact us here at This email address is being protected from spambots. You need JavaScript enabled to view it. .

310 558 91 17

What do I need to do to obtain the RUT?

Under construction.

What is the RUT?

What is the RUT?

It is the Single Tax Registry, through which individuals and legal entities are identified before the National Tax and Customs Directorate (DIAN).

I received a letter, email or request from the DIAN

I received a letter, email or request from the DIAN. What should I do?

First, attention must be paid to requests made by the DIAN. Normally, when this entity finds that a taxpayer must comply with a tax obligation, it sends a message or invitation to file an income tax return, asking the person to comply with what is requested in the message.

When the DIAN issues these communications, in most cases they must be complied with or answered because the DIAN has performed the corresponding information cross-checks to determine whether the person is required to comply with one or more obligations.

If you received a physical letter, an email message or even a text message to your cell phone, the most advisable course is to contact us so we can determine the authenticity of the message and tell you the steps to follow. It is very important to emphasize that at the first notification it is better to act immediately. If you do not respond, the DIAN continues notifying you through its legal procedure, making the obligation increasingly expensive to comply with.

For example, if you are required to file an income tax return, it is better to do so. In many cases the tax payable is zero, but the penalty for not filing or for filing late in 2022 is $380,000.

The consultation with us to determine your obligation is free.

Phone: 310 558 91 17 - 313 821 48 03, or submit your inquiry through this page.

How much do I have to pay to register my business?

The costs associated with creating and/or formalizing companies in Bogotá are determined by the rates set in Decree 650 of 1996 and the ordinances of the Cundinamarca Assembly 216 of 2014 and 015 of 2016. For example, for the creation of an SAS, the registration tax is 0.7% of the subscribed capital.

Decree 650 of 1996, issued on April 3 and published in Official Gazette No. 42,761 of April 9, 1996, partially regulated Law 223 of 1995.

Chapter I. Registration Tax.

Article 1. Acts, contracts and legal transactions subject to registration tax. Registrations of documents containing acts, orders, contracts or legal transactions in which private parties are parties or beneficiaries and which, by law, must be registered with Chambers of Commerce or Public Instrument Registry Offices are subject to registration tax under Law 223 of 1995.

Article 9. Tax rate for acts, contracts or legal transactions with a stated value. All acts, contracts or legal transactions with a stated value that are subject to registration tax and must be registered with Public Instrument Registry Offices are taxed at rates between 0.5% and 1%, determined by the corresponding departmental assembly at the initiative of the Governor. Likewise, all acts, contracts or legal transactions with a stated value that are subject to registration tax and must be registered with Chambers of Commerce are taxed at rates between 0.3% and 0.7%, determined by the corresponding departmental assembly at the initiative of the Governor.

Ordinance No. 216/2014, whereby the Revenue Statute of the Department of Cundinamarca is issued, certain powers are granted to the Governor of the Department and other provisions are enacted, establishes the registration tax rates. For acts, contracts or legal transactions with a stated value subject to registration with Chambers of Commerce, the rate is 0.7%.

In addition to the registration tax, the following must be paid at the Chamber:

Concept | Value

Registration in the commercial registry of acts and documents | $45,000

Registration of books in the commercial registry | $15,000

Commercial registration certificate | $3,100

Certificate of existence and legal representation | $6,200

RUES form | $6,200

| In summary, when creating an SAS with subscribed capital of $10,000,000, the following must be paid: | Concept |

|---|---|

| Amount payable | Registration tax |

| $70,000 | Chamber registration fees |

| $45,000 | RUES form |

| $6,200 | Certificate of existence and legal representation |

| $6,200 | Estimated total |

If you are thinking about creating or formalizing your company, contact us and we will help you.

| $127,400 | Remember: the first consultation is FREE. Request it here. |

|---|---|

| 310 558 9117 – 313 821 48 03 | Am I required to keep accounting records? |

| Under construction. Please contact us for more information. Phone: 3105589117. | Frequently asked questions |

| Single Registry of Beneficial Owners (RUB). | If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step. |

| Schedule an appointment | General contact |

| Total estimado | $127.400 |

Si esta pensando en crear o formalizar su empresa, Contáctenos y nosotros le ayudamos

Recuerde, la primera consulta es GRATIS. Solicítela aquí

310 558 9117– 313 821 48 03

¿Estoy obligado a llevar contabilidad?

En construcción. Por favor contáctenos para mayor informacion. Tel 3105589117

- Details

- Category: Resources

- Hits: 61

Accounting Bogotá

My Area

Information organized to consult the topic and review the main points more clearly.