New ICA Rates in Bogotá as of 2022

- Details

- Category: Tax advisory

- Hits: 25

Accounting Bogotá

New ICA rates in Bogotá as of 2022

With the issuance of District Agreement 780 of November 6, 2020, new rates were created for the Industry and Commerce Tax (ICA) in the city of Bogotá.

Key information

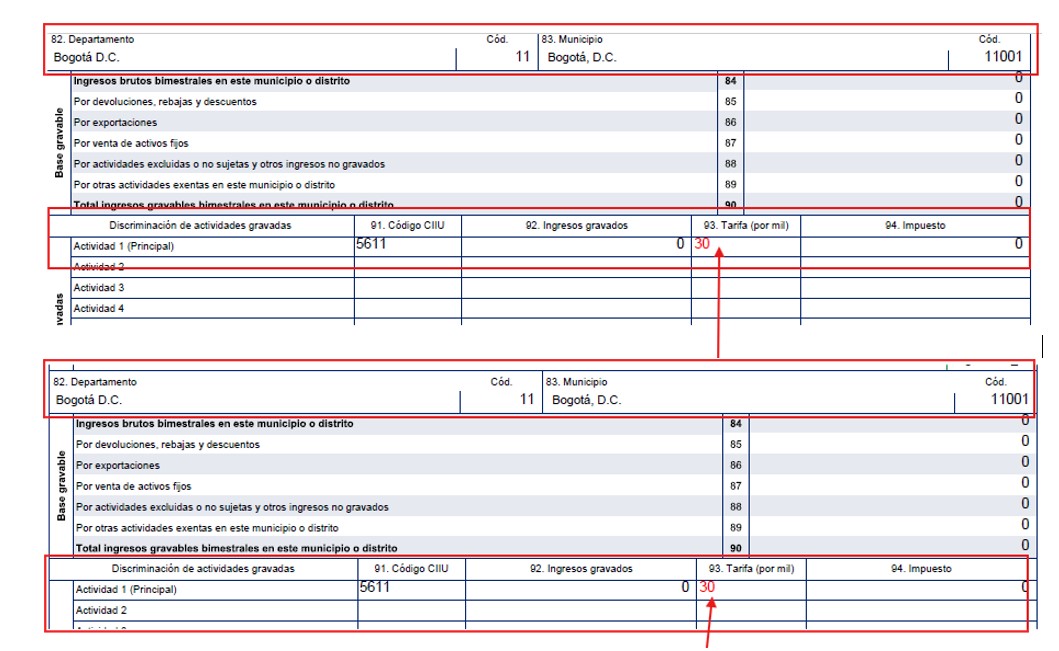

Article 6 of the Agreement modifies the Industry and Commerce Tax rate, starting in taxable year 2022, for industrial, service and financial activities. Among others, professional consulting activities and services provided by contractors, builders and developers increased from 6.9 to 8.66 per thousand, while consulting services in the practice of a liberal profession decreased from 9.66 to 7.66 per thousand as of 2022.

Likewise, Article 5 establishes a temporary increase in ICA rates for taxable year 2021 for those who increased their income during the epidemiological situation caused by Coronavirus (COVID-19).

Later, Resolution No. SDH-000265 of April 13, 2021 adopted and updated the classification of economic activities (CIIU) and defined the ICA rates for all taxable activities in Bogotá.

It resolves:

ARTICLE 1. To establish the classification of economic activities for purposes of the administration, control, collection and determination of the Industry and Commerce Tax in the Capital District of Bogotá. See here the ICA activities and rates for 2022, 2023, 2024, 2025 and 2026.For the correct application of Bogotá’s Industry and Commerce Tax, the District Treasury Secretariat (SDH) has published the ICA Guide, which undoubtedly helps clarify several questions when applying the tax.

These rates are important in order to apply the correct rate in ICA withholding processes. Learn here who the withholding agents are for Bogotá’s Industry and Commerce Tax and how the system operates.

According to the dynamics of how ICA withholding operates among taxpayers under Article 2, “Operation of the System,” of Resolution DDI-000305 of January 16, 2020 on withholding agents, Bogotá’s ICA Large Taxpayers are subject to withholding only by public entities and by large taxpayers designated by the DIAN. For 2026, Resolution DDI 029334 of October 31, 2025 designated Bogotá’s ICA Large Taxpayers.The withholding system is governed, as applicable to the nature of the Industry and Commerce Tax, by the specific rules adopted by the Capital District and the general withholding system rules applicable to income tax and complementary taxes.

To ensure efficient collection of the Industry and Commerce Tax, the Bogotá District Tax Directorate issued Resolution DDI-000305 of January 16, 2020, designating withholding agents for the Industry and Commerce Tax.

The following are withholding agents:

Public law entities.

Those classified as large taxpayers by the DIAN.

Those designated as withholding agents by resolution of the district tax director.

Intermediaries or third parties that participate in economic operations in which ICA withholding is generated.

Consortiums and temporary unions when they make payments or credits to account to taxpayers under the ordinary and/or preferential ICA regime in taxed transactions within the Capital District.

Ordinary ICA regime taxpayers when the payment beneficiary belongs to the preferential regime and carries out taxed activities within the Capital District.

As of July 1, 2004, ordinary ICA regime taxpayers must also apply ICA withholding to beneficiaries registered under the ordinary regime if they are independent professionals and participate in taxed activities within Bogotá.

Circumstances under which withholding is NOT applied:

Payments or credits to account made to non-ICA taxpayers.

Payments or credits to account that are not subject to tax or are exempt.

When the beneficiary of the payment is a public law entity.

When the beneficiary is classified as a large taxpayer by the DIAN and is an ICA filer in Bogotá, except when the withholding agent is a public entity.

Resources from the capitation payment unit of the subsidized and contributory regimes of the General Social Security Health System.

Payments for public utilities.

If there is a special taxable base, withholding is applied on that base.

The ICA withholding rate is the rate corresponding to the respective activity. When the party subject to withholding does not report the activity or it cannot be established, the withholding rate is the maximum rate in force for the Industry and Commerce Tax within the taxable period, and the transaction is taxed at that same rate.

Minimum bases to apply withholding for 2026:

Minimum withholding bases for 2026 (UVT value: $52,374)

Concept | Base in UVT | Base in pesos

| Purchases | 27 UVT | $1,414,098 |

|---|---|---|

| Source: Bogotá District Treasury Secretariat - ICA. | If this information helped you, leave us your comments here. | We provide tax advisory services. |

| Contact us; the first consultation is free: Tel / WhatsApp 310 558 91 17 – 313 821 48 03 | If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step. | Schedule an appointment |

General contactSecretaría Distrital de Hacienda de Bogotá - ICA.

Si la anterior informacion les ayudó, déjenos sus comentarios aquí.

Prestamos asesoría en materia tributaria.