Income Tax Return Advisory

- Details

- Category: Tax advisory

- Hits: 36

Accounting Bogotá

Income Tax Return Advisory

Our income tax return advisory service, including the requirements for 2025-2026, allows us to identify the tax and fiscal obligations that apply and that, if unknown, may lead to non-compliance with formal and substantive obligations. Formal obligations refer to the duties that must be fulfilled in order to comply with substantive obligations. Examples of formal obligations include registration in the RUT, registration in the Tax Information Registry (RIT), and similar duties. Substantive obligations include, for example, filing income tax, VAT, ICA and other returns.

Income Tax Return Advisory

These returns have minimum requirements to ensure their effectiveness, that is, to be considered properly filed. Otherwise, the return may be deemed ineffective, generating penalties and interest, which in many cases may be higher than the tax itself.

Proper advisory support can help you avoid excessive tax payments, penalties and interest.

For 2026, the DIAN minimum penalty is 10 UVT, that is, $524,000. For example, a return with $10,000 of tax payable, if not filed correctly, may turn into an amount payable greater than $524,000. For this purpose, the filing deadlines under the DIAN 2026 tax calendar must be taken into account.

Request advice with no obligation here, schedule an advisory appointment here, call 310 558 91 17, or check whether you must file an income tax return here.

New 2026 rates for Bogotá’s SIMPLE regime

Increase in ICA in Bogotá for SIMPLE regime taxpayers in 2026.

For 2026, Bogotá increased the ICA component rates for taxpayers registered under the Simple Taxation Regime.

The change was established in Article 44 of Bogotá Council Agreement 1019 of 2025 and applies to the fiscal year from January 1 to December 31, 2026.

It is important to clarify that not all SIMPLE taxpayers are subject to a rate of 30 per thousand. The rate depends on the economic activity group established in Article 908 of the Tax Code.

Previous and new rates

Previously, under Agreement 780 of 2020, Bogotá applied SIMPLE ICA rates between 5 and 12 per thousand, depending on whether the activity was industrial, commercial or service-based.

For 2026, the new rates are:

| SIMPLE Group | Main activities | Approximate previous rate | New 2026 rate |

|---|---|---|---|

| Group 1 | Small stores, minimarkets and hair salons | 6 to 12 per thousand | 12 per thousand |

| Group 2 | Commerce, industry, technical services, construction and other activities | 5 to 12 per thousand | 16 per thousand |

| Group 3 | Sale of food and beverages, and transportation | 6 to 12 per thousand | 30 per thousand |

| Group 3 SIC | Professional services, consulting and liberal professions | 6 to 12 per thousand | 30 per thousand |

| Group 6 | Recycling, material recovery and waste collection | Up to 12 per thousand | 16 per thousand |

Most affected sectors

The most affected sectors are those moving to the 30 per thousand rate, especially:

Restaurants, cafés and establishments selling food and beverages.

Transportation.

Professional services.

Consulting.

Liberal professions.

The impact may be significant because some taxpayers who previously paid between 6 and 12 per thousand would now pay 30 per thousand for the ICA component in Bogotá.

For example, on taxable income of $100,000,000:

| Rate | Approximate ICA on $100,000,000 |

|---|---|

| 12 per thousand | $1,200,000 |

| 30 per thousand | $3,000,000 |

The difference would be $1,800,000 for every $100,000,000 of taxable income in Bogotá.

Recommendations

SIMPLE taxpayers in Bogotá should:

Review which group under Article 908 of the Tax Code they are classified in.

Verify whether all their income actually corresponds to Bogotá or whether part of the activity is carried out in other municipalities.

Simulate whether remaining under the SIMPLE regime continues to be convenient.

Adjust budgets, advances and prices for 2026.

Avoid changing the economic activity only to seek a lower rate if it does not correspond to the business reality.

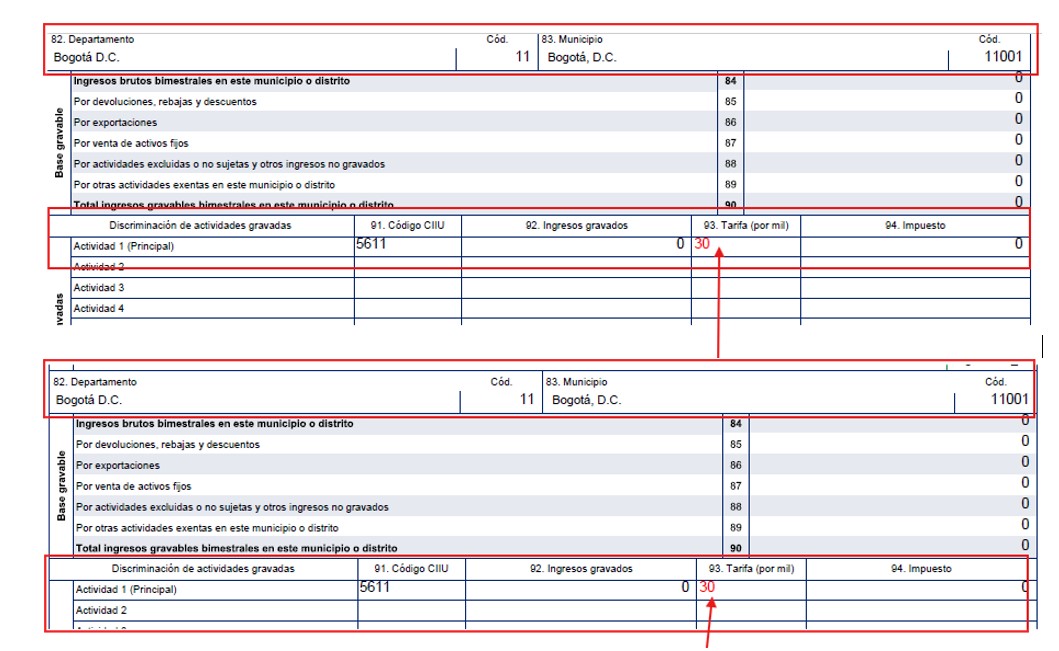

The images of two advances filed for the January-February 2026 bimonthly period show the 30 per thousand rate for activity 5611, restaurant services, and activity 7020, consulting services, which are among the most affected by this increase.

Through Press Release 074 of May 19, 2026, the DIAN clarified that the increase in Bogotá’s consolidated ICA component does not mean that the national rates of the Simple Taxation Regime increased.

What happened is that Bogotá, through District Agreement 1019 of 2025, increased the consolidated ICA component rate for some SIMPLE taxpayers, especially those in group 3 and group 3 SIC, from 10 per thousand to 30 per thousand. These groups mainly include the sale of food and beverages, transportation, professional services, consulting and scientific activities.

So did SIMPLE increase?

Not necessarily. According to the DIAN, the general SIMPLE rate was not increased by the National Government. What changes is the internal distribution of the tax.

The SIMPLE regime is made up of several elements, including:

The national SIMPLE component, administered by the DIAN.

The territorial ICA component, which belongs to the municipality or district.

When Bogotá’s ICA component increases, the portion corresponding to the national SIMPLE component decreases. Therefore, the DIAN indicated that the change does not increase the total value of the RST advance; it represents an internal redistribution among the components of the consolidated tax.

Practical example

Suppose a group 3 taxpayer in Bogotá has bimonthly income of $100,000,000 and a consolidated SIMPLE rate of 3.4%.

| Concept | Before the Bogotá ICA increase | After the Bogotá ICA increase |

|---|---|---|

| Taxpayer’s bimonthly income | $100,000,000 | $100,000,000 |

| SIMPLE regime group | Group 3 | Group 3 |

| Consolidated SIMPLE rate in the example | 3.40% | 3.40% |

| Total SIMPLE tax | $3,400,000 | $3,400,000 |

| Bogotá ICA rate | 10 per thousand | 30 per thousand |

| Bogotá ICA component | $1,000,000 | $3,000,000 |

| National DIAN component | $2,400,000 | $400,000 |

| Total payable on the SIMPLE receipt | $3,400,000 | $3,400,000 |

Conclusion

The increase in SIMPLE ICA in Bogotá for 2026 is real, but it does not apply equally to everyone. The rates are 12, 16 or 30 per thousand, depending on the activity group.

The greatest impact will fall on taxpayers providing professional services, consulting, restaurants, food establishments and transportation, which are subject to the 30 per thousand rate.

It cannot be said that the SIMPLE tax in general increased. The correct statement is that, in Bogotá, the consolidated ICA component increased for certain groups within the SIMPLE regime.

Consequently, the general SIMPLE rate remains the same, but the distribution of the payment changes: Bogotá receives a larger share through ICA and the DIAN receives a smaller share through the national component.

For some taxpayers who already filed the SIMPLE advance for the January-February 2026 bimonthly period, this increase was not reflected.

If you have comments, contact us.

If this information helped you, leave us your comments here.We provide tax advisory services..

Contact us; the first consultation is free: Tel / WhatsApp 310 558 91 17 – 313 821 48 03

Income tax return calendar for individuals, taxable year 2025

If you are required to file your income tax return for taxable year 2025, which is filed in 2026 according to the last two digits of your NIT or citizenship ID number, the following are the maximum dates for filing the corresponding return. Remember, however, that preparing the return takes time and must be done with special care, without rushing. Therefore, it is recommended to begin the process now in coordination with your accountant and have it ready at least three days before the deadline.

Who must file an income tax return for 2025 starting August 12, 2026.

Individuals not required to file an income tax return in 2026 for taxable year 2025.

All individuals and estates that meet the following conditions are not required to file an income tax return for taxable year 2025.

To avoid being required to file an income tax return for taxable year 2025, all these conditions must be met:

Condition | Limit or requirement

| Not being responsible for VAT | Qualitative requirement |

|---|---|

| Gross assets at the end of the taxable year | Up to 4,500 UVT ($224,096,000) |

| Gross income | Less than 1,400 UVT ($69,719,000) |

| Credit card consumption | Up to 1,400 UVT ($69,719,000) |

| Total purchases and consumption | Up to 1,400 UVT ($69,719,000) |

| Bank deposits, deposits or financial investments | Up to 1,400 UVT ($69,719,000) |

| Minimum late-filing penalty | $524,000 |

| If you do not meet any of the above conditions, you must file the income tax return for 2025. | Documents required to prepare the income tax return for taxable year 2025. |

In coordination with your accountant, you must provide the following documents, among others, as a basis for preparing the income tax return:

A copy of the certificate of registration in the Single Tax Registry (RUT), duly updated.

Income tax returns for the last two taxable years.

Documents to determine assets:

Certificates or statements showing the balances of savings and checking accounts issued by financial institutions.

Investment certificates issued by the entities where the investment was made, such as CDs, bonds, trust rights, mandatory investments and others.

Property tax declaration or account statement for real estate owned.

Deeds of acquisition for real estate and/or certificates from the public registry.

Vehicle purchase invoice or document showing the acquisition value of vehicles and vehicle tax account statement.

List of furniture, fixtures, machinery and equipment, at acquisition value plus additions and improvements.

Technical appraisal certificate for intangible assets such as goodwill, copyright, industrial, literary, artistic and scientific property, and others.

Bills of exchange, promissory notes and other documents supporting accounts receivable and obligations or debts, in accordance with legal requirements.

Documents to determine income:

Certificate of employment income and withholdings.

Certificates of compensation for work accidents or illness, maternity, worker burial expenses, death insurance and death compensation for members of the Military Forces and National Police.

Certificates for dividends and shares received during the year.

Certificates for pension substitute indemnities or refunds of pension savings balances.

Certificates of income for fees, commissions and services.

Certificates of financial returns paid during the year, issued by the corresponding entities.

Certificates of dividends and shares received during the year, issued by the companies of which you are a partner or shareholder.

Certificates of income received during the year from profits distributed by liquidated companies.

Certificates of payments for meals made by your employer.

Certificates of payment of life insurance indemnities.

Documents to determine payments that constitute deductions:

Certificate of interest payments on loans for housing acquisition.

Certificates for mandatory health payments and prepaid medical plans.

Certificates for investments in new irrigation plantations, wells, silos, detention centers, maintenance and conservation of audiovisual works, bookstores, film projects and others.

Certificates for donations to the Nation, departments, municipalities, districts, Indigenous territories and others.

List of expense invoices, indicating the total value.

List of payments made to employees for salaries, bonuses, vacation, severance pay and others.

Contact us and we will prepare your return.

Phone: 310 558 91 17 - 313 821 48 03

Withholding Tax

Withholding tax is not a tax in itself; it is a mechanism through which the government collects a tax in advance, that is, before the filing deadline. You may be a withholding agent without knowing it, or withholding may be applied to you and you may not know what to do with it. In any of these cases, it is necessary to understand the reason for the situation in order to ensure proper regulatory compliance and avoid high penalties for non-compliance. If you are a merchant and withholding tax was applied to you, meaning you were paid less, you may not have to lose that amount; we will tell you how to proceed in these cases.

It should be noted that withholding tax must be paid within the corresponding deadlines. If it is not paid, the filing will be considered not made, and therefore it must be filed again and the corresponding penalties and interest must be calculated.

+57 310 558 91 17 - +57 313 821 48 03

If you need more information, advice or guidance, request an appointment here.

Individual income tax and calendar

How to know whether I must file an income tax return.Income tax return calendar for individuals, taxable year 2025.