Withholding Tax

- Details

- Category: Tax advisory

- Hits: 21

Accounting Bogotá

Withholding Tax

Withholding tax is not a tax in itself; it is a mechanism through which the government collects a tax in advance, that is, before the filing deadline. You may be a withholding agent without knowing it, or withholding may be applied to you and you may not know what to do with it. In any of these cases, it is necessary to understand the reason for the situation in order to ensure proper regulatory compliance and avoid high penalties for non-compliance. If you are a merchant and withholding tax was applied to you, meaning you were paid less, you may not have to lose that amount; we will tell you how to proceed in these cases. It should be noted that withholding tax must be paid within the corresponding deadlines. If it is not paid, the filing will be considered not made, and therefore it must be filed again and the corresponding penalties and interest must be calculated.

Withholding Tax

+57 310 558 91 17 - +57 313 821 48 03

If you need more information, advice or guidance, request an appointment here.New 2026 rates for Bogotá’s SIMPLE regime

Increase in ICA in Bogotá for SIMPLE regime taxpayers in 2026.

For 2026, Bogotá increased the ICA component rates for taxpayers registered under the Simple Taxation Regime.

The change was established in Article 44 of Bogotá Council Agreement 1019 of 2025 and applies to the fiscal year from January 1 to December 31, 2026.

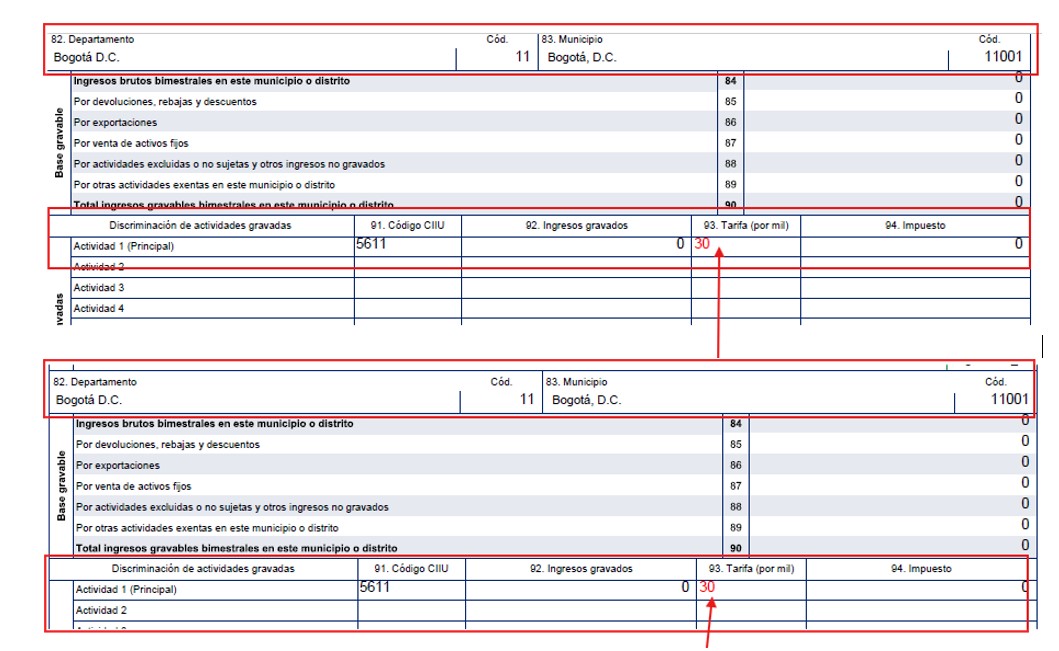

It is important to clarify that not all SIMPLE taxpayers are subject to a rate of 30 per thousand. The rate depends on the economic activity group established in Article 908 of the Tax Code.

Previous and new rates

Previously, under Agreement 780 of 2020, Bogotá applied SIMPLE ICA rates between 5 and 12 per thousand, depending on whether the activity was industrial, commercial or service-based.

For 2026, the new rates are:

SIMPLE Group | Main activities | Approximate previous rate | New 2026 rate

| Group 1 | Small stores, minimarkets and hair salons | 6 to 12 per thousand | 12 per thousand |

|---|---|---|---|

| Group 2 | Commerce, industry, technical services, construction and other activities | 5 to 12 per thousand | 16 per thousand |

| Group 3 | Sale of food and beverages, and transportation | 6 to 12 per thousand | 30 per thousand |

| Group 3 SIC | Professional services, consulting and liberal professions | 6 to 12 per thousand | 30 per thousand |

| Group 6 | Recycling, material recovery and waste collection | Up to 12 per thousand | 16 per thousand |

| Most affected sectors | The most affected sectors are those moving to the 30 per thousand rate, especially restaurants, cafés, food and beverage establishments, transportation, professional services, consulting and liberal professions. | The impact may be significant because some taxpayers who previously paid between 6 and 12 per thousand would now pay 30 per thousand for the ICA component in Bogotá. | For example, on taxable income of $100,000,000: |

Rate | Approximate ICA on $100,000,000

12 per thousand | $1,200,000

30 per thousand | $3,000,000

The difference would be $1,800,000 for every $100,000,000 of taxable income in Bogotá.

Recommendations

SIMPLE taxpayers in Bogotá should review which group under Article 908 of the Tax Code they are classified in, verify whether all income actually corresponds to Bogotá or whether part of the activity is carried out in other municipalities, simulate whether remaining under the SIMPLE regime continues to be convenient, adjust budgets, advances and prices for 2026, and avoid changing the economic activity only to seek a lower rate if it does not correspond to the business reality.

The images of two advances filed for the January-February 2026 bimonthly period show the 30 per thousand rate for activity 5611, restaurant services, and activity 7020, consulting services, which are among the most affected by this increase.

Through Press Release 074 of May 19, 2026, the DIAN clarified that the increase in Bogotá’s consolidated ICA component does not mean that the national rates of the Simple Taxation Regime increased.

What happened is that Bogotá, through District Agreement 1019 of 2025, increased the consolidated ICA component rate for some SIMPLE taxpayers, especially those in group 3 and group 3 SIC, from 10 per thousand to 30 per thousand. These groups mainly include the sale of food and beverages, transportation, professional services, consulting and scientific activities.

| So did SIMPLE increase? | Not necessarily. According to the DIAN, the general SIMPLE rate was not increased by the National Government. What changes is the internal distribution of the tax. |

|---|---|

| The SIMPLE regime is made up of several elements, including the national SIMPLE component administered by the DIAN and the territorial ICA component belonging to the municipality or district. When Bogotá’s ICA component increases, the portion corresponding to the national SIMPLE component decreases. Therefore, the DIAN indicated that the change does not increase the total value of the RST advance; it represents an internal redistribution among the components of the consolidated tax. | Practical example |

| Suppose a group 3 taxpayer in Bogotá has bimonthly income of $100,000,000 and a consolidated SIMPLE rate of 3.4%. | Concept |

Taxpayer’s bimonthly income | $100,000,000 | $100,000,000

SIMPLE regime group | Group 3 | Group 3

Consolidated SIMPLE rate in the example | 3.40% | 3.40%

Total SIMPLE tax | $3,400,000 | $3,400,000

Bogotá ICA rate | 10 per thousand | 30 per thousand

Bogotá ICA component | $1,000,000 | $3,000,000

National DIAN component | $2,400,000 | $400,000

Total payable on the SIMPLE receipt | $3,400,000 | $3,400,000

Conclusion

The increase in SIMPLE ICA in Bogotá for 2026 is real, but it does not apply equally to everyone. The rates are 12, 16 or 30 per thousand, depending on the activity group.

The greatest impact will fall on taxpayers providing professional services, consulting, restaurants, food establishments and transportation, which are subject to the 30 per thousand rate.

It cannot be said that the SIMPLE tax in general increased. The correct statement is that, in Bogotá, the consolidated ICA component increased for certain groups within the SIMPLE regime.

Consequently, the general SIMPLE rate remains the same, but the distribution of the payment changes: Bogotá receives a larger share through ICA and the DIAN receives a smaller share through the national component.

For some taxpayers who already filed the SIMPLE advance for the January-February 2026 bimonthly period, this increase was not reflected.

If you have comments, contact us.

If this information helped you, leave us your comments here.

We provide tax advisory services.

Contact us; the first consultation is free: Tel / WhatsApp 310 558 91 17 – 313 821 48 03

Income tax return calendar for individuals, taxable year 2025

| Before the Bogotá ICA increase | After the Bogotá ICA increase | If you are required to file your income tax return for taxable year 2025, which is filed in 2026 according to the last two digits of your NIT or citizenship ID number, the maximum dates for filing the corresponding return apply. Remember that preparing the return takes time and must be done carefully, without rushing. It is recommended to begin the process now with your accountant and have it ready at least three days before the deadline. |

|---|---|---|

| Individuals not required to file an income tax return in 2026 for taxable year 2025. | All individuals and estates that meet all of the following conditions are not required to file an income tax return for taxable year 2025: | Condition |

| Limit or requirement | Not being responsible for VAT | Qualitative requirement |

| Gross assets at the end of the taxable year | Up to 4,500 UVT ($224,096,000) | Gross income |

| Less than 1,400 UVT ($69,719,000) | Credit card consumption | Up to 1,400 UVT ($69,719,000) |

| Total purchases and consumption | Up to 1,400 UVT ($69,719,000) | Bank deposits, deposits or financial investments |

| Up to 1,400 UVT ($69,719,000) | Minimum late-filing penalty | $524,000 |

| If you do not meet any of the above conditions, you must file the income tax return for 2025. | Documents required to prepare the income tax return for taxable year 2025 include, among others, the updated RUT certificate, income tax returns from the last two taxable years, documents supporting assets, income and deductions, bank statements, investment certificates, property and vehicle information, employment income and withholding certificates, certificates for dividends, fees, financial returns, donations, health payments, housing loan interest, expense invoices and payments made to employees. | Contact us and we will prepare your return. |

| Phone: 310 558 91 17 - 313 821 48 03 | Income Tax Return Advisory | Our income tax return advisory service, including the requirements for 2025-2026, allows us to identify the tax and fiscal obligations that apply and that, if unknown, may lead to non-compliance with formal and substantive obligations. Formal obligations refer to the duties that must be fulfilled in order to comply with substantive obligations. Examples of formal obligations include registration in the RUT, registration in the Tax Information Registry (RIT), and similar duties. Substantive obligations include, for example, filing income tax, VAT, ICA and other returns. |

These returns have minimum requirements to ensure their effectiveness, that is, to be considered properly filed. Otherwise, the return may be deemed ineffective, generating penalties and interest, which in many cases may be higher than the tax itself.

Proper advisory support can help you avoid excessive tax payments, penalties and interest.

For 2026, the DIAN minimum penalty is 10 UVT, that is, $524,000. For example, a return with $10,000 of tax payable, if not filed correctly, may turn into an amount payable greater than $524,000. The filing deadlines under the DIAN 2026 tax calendar must be taken into account.

Request advice with no obligation here, schedule an advisory appointment here, call 310 558 91 17, or check whether you must file an income tax return here.

Withholding Tax

Can withholding tax be filed without payment?

If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step.

Schedule an appointmentGeneral contact.

Prestamos asesoría en materia tributaria.

Contáctenos, la primera es gratis: Tel WA 310 558 91 17 – 313 821 48 03

Calendario de declaración de renta para personas naturales, año gravable 2025

Si está obligado a presentar su declaración de Renta por el año gravable 2025 que se presenta en 2026 de acuerdo con los dos últimos dígitos de su NIT o Cédula de ciudadanía, las siguientes son las fechas máximas para presentar la respectiva declaración. Pero recuerde, que el proceso de elaboración toma tiempo y se debe elaborar con especial cuidado, sin afanes, por lo que se recomienda iniciar el proceso desde ya en coordinación con su Contador y tenerla lista por lo menos tres días antes de la fecha de vencimiento.

Quiénes deben presentar declaración de renta del año 2025 a partir del 12 de agosto de 2026

NO obligados a declarar renta en 2026 por el año gravable 2025

Todas las personas naturales y sucesiones ilíquidas que cumplan las siguientes condiciones, NO deben presentar declaración de renta por el año gravable 2025:

Para no estar obligado a declarar renta por el año gravable 2025 deben cumplirse todas estas condiciones:

| Condición | Tope o requisito |

|---|---|

| No ser responsable del impuesto a las ventas IVA | Requisito cualitativo |

| Patrimonio bruto al cierre del año gravable | Hasta 4.500 UVT ($224.096.000) |

| Ingresos brutos | Inferiores a 1.400 UVT ($69.719.000) |

| Consumos con tarjeta de crédito | Hasta 1.400 UVT ($69.719.000) |

| Compras y consumos totales | Hasta 1.400 UVT ($69.719.000) |

| Consignaciones, depósitos o inversiones financieras | Hasta 1.400 UVT ($69.719.000) |

| Sanción mínima por extemporaneidad | $524.000 |

Si no cumple alguna de las anteriores condiciones, debe presentar declaración de renta del año 2025.

Documentos Necesarios para Elabora la Declaración de Renta Año Gravable 2025.

En coordinación con su Contador, deberá aportar los siguientes documentos entre otros como base para elaborar la declaración de renta.

Copia del certificado de inscripción en el Registro Único Tributario –RUT– debidamente actualizado.

Declaración de renta de los 2 últimos años gravables.

Documentos para determinar el patrimonio

Certificados o extractos de los saldos de las cuentas de ahorro y corrientes emitidos por las entidades financieras.

Certificados de las inversiones emitidos por las entidades donde se constituyó la inversión, por ejemplo: CDT, bonos, derechos fiduciarios, inversiones obligatorias, entre otras.

Declaración o estado de cuenta del impuesto predial de los bienes inmuebles que posea.

Escrituras de adquisición de los bienes inmuebles y/o certificados de instrumentos públicos.

Factura de compra o documento donde conste el valor de adquisición de los vehículos y estado de cuenta del impuesto de vehículos.

Relación de los muebles, enseres, máquinaria y equipo, por su valor de adquisición más adiciones y mejoras.

Certificado de avalúo técnico de los bienes incorporales tales como good will, derechos de autor, propiedad industrial, literaria, artística, científica y otros.

Letras, pagarés y demás documentos que respalden cuentas por cobrar y obligaciones o deudas, conforme a los requisitos de ley.

Documentos para determinar los ingresos

Certificado de ingresos y retenciones laborales.

Certificado de indemnizaciones por accidentes de trabajo o de enfermedad, maternidad, gastos de entierro del trabajador, seguro por muerte y compensaciones por muerte de miembros de las Fuerzas Militares y Policía Nacional.

Certificados por concepto de dividendos y participaciones recibidos en el año.

Certificados de indemnizaciones sustitutivas de la pensión o devoluciones de saldos de ahorro pensional.

Certificados de ingresos por concepto de honorarios, comisiones y servicios.

Certificados de rendimientos financieros pagados durante el año, expedidos por las entidades correspondientes.

Certificado de dividendos y participaciones recibidos durante el año, expedidos por las sociedades de las cuales es socio o accionista.

Certificados de ingresos recibidos durante el año por concepto de utilidades repartidas por sociedades liquidadas.

Certificados de pagos por concepto de alimentación, efectuados por su empleador.

Certificados de pago de indemnizaciones por seguros de vida.

Documentos para determinar los pagos que constituyen deducciones

Certificado de pagos de intereses por préstamos para adquisición de vivienda.

Certificados por pagos de salud obligatoria y medicina prepagada.

Certificados por inversiones en nuevas plantaciones de riegos, pozos, silos, centros de reclusión, en mantenimiento y conservación de obras audiovisuales, en librerías, proyectos cinematográficos y otros.

Certificados por donaciones a la Nación, departamentos, municipios, distritos, territorios indígenas y otros.

Relación de facturas de gastos, indicando el valor total.

Relación de los pagos efectuados a sus empleados por concepto de sueldos, bonificaciones, vacaciones, cesantías y otros.

Consultenos y elaboraremos su declaración.

Tel 310 558 91 17 - 313 821 48 03

Asesoría en Declaración de Renta

Nuestra asesoría en declaración de renta. (Consulte aquí los requisitos para el año 2025-2026) permite la identificación de las obligaciones que se tienen de tipo tributario y fiscal que al no conocerlas, trae como consecuencia el incumplimiento de obligaciones formales y sustanciales. Las primeras se refieren a los deberes que se debe atender con el fin de cumplir con las segundas, es decir con las sustanciales. Son ejemplo de obligaciones formales la inscripción en el RUT, Registro de Información Tributaria RIT, etc. Las obligaciones sustanciales son por ejemplo las declaración de Renta, IVA, ICA, etc.

Estas declaraciones tienen unos requisitos mínimos para asegurar su eficacia, es decir, que se den por presentadas correctamente, de lo contrario se puede incurrir en ineficacia de las mismas con la consecuente generación de sanciones e intereses, que en muchos casos es mayor que el mismo impuesto generado.

Una adecuada asesoría le puede evitar un pago excesivo por impuestos, así como de sanciones e intereses.

Para 2026 la sanción mínima de la DIAN es de 10 UVTs, es decir $524.000. Así por ejemplo una declaración con impuesto a pagar de $10.000 si no se presenta en debida forma puede convertirse en un valor por pagar superior a $524.000. Para lo anterior se debe tener en cuenta las fechas límites según el Calendario DIAN 2026 para el año 2026 de la DIAN.

Pida una asesoria sin compromiso Aquí ó Programe una cita de asesoría Aquí Tel 310 558 91 17 o verifique si debe Declarar Renta Aquí