Single Registry of Beneficial Owners (RUB)

- Details

- Category: Resources

- Hits: 20

Accounting Bogotá

Single Registry of Beneficial Owners (RUB)

Within the framework of the fight against corruption, money laundering, terrorism financing and tax evasion, the National Government, through Article 16 of Law 2155 of September 14, 2021, modified Article 631-5 of the Tax Code, defining the concept of Beneficial Owner. Article 17 created the Single Registry of Beneficial Owners (RUB) as part of the Single Tax Registry (RUT). Through this registry, all entities with a RUT and Non-Legal-Entity Structures (SIESPJ) and similar structures not required to register in the RUT must provide information about the beneficial owners of those entities.

Key information

A beneficial owner is defined as “the natural person or persons who ultimately own or control, directly or indirectly, a client and/or the natural person on whose behalf a transaction is carried out. It also includes the natural person or persons who exercise effective and/or final control, directly or indirectly, over a legal entity or another structure without legal personality.”

A) The following are beneficial owners of a legal entity:

1. The natural person who, acting individually or jointly, directly or indirectly owns five percent (5%) or more of the capital or voting rights of the legal entity, and/or benefits from five percent (5%) or more of the assets, returns or profits of the legal entity; and

2. The natural person who, acting individually or jointly, exercises control over the legal entity by any means other than those established in the previous paragraph; or

3. When no natural person is identified under the two previous paragraphs, the natural person who holds the position of legal representative must be identified, unless there is another natural person with greater authority in relation to the management or direction functions of the legal entity.

B) The following natural persons are beneficial owners of a structure without legal personality or a similar structure:

1. Settlor, trustor, founder or similar or equivalent position;

2. Trustee or similar or equivalent position;

3. Trust committee, financial committee or similar or equivalent position;

4. Beneficiary or conditional beneficiary; and

5. Any other natural person who exercises effective and/or final control, or who has the right to enjoy and/or dispose of the assets, benefits, results or profits.

Parties required to file the RUB and deadlines:

Resolution 164 of December 27, 2021 regulated Articles 631-5 and 631-6 of the Tax Code and adopted the technical annex to that Resolution, defining the characteristics and content of the file through which Beneficial Owners are reported.

Law 2195 of January 18, 2022 adopted measures on transparency, prevention and the fight against corruption. It establishes administrative and sanctioning liability against legal entities and branches of foreign companies for acts of corruption, as well as administrative sanctions and the grading of sanctions applicable to those persons. It also establishes the obligation to implement transparency and business ethics programs that include internal audit mechanisms and rules; establishes penalties for violations of prohibitions related to commercial books; and identifies the entities that have access to the Single Registry of Beneficial Owners (RUB).

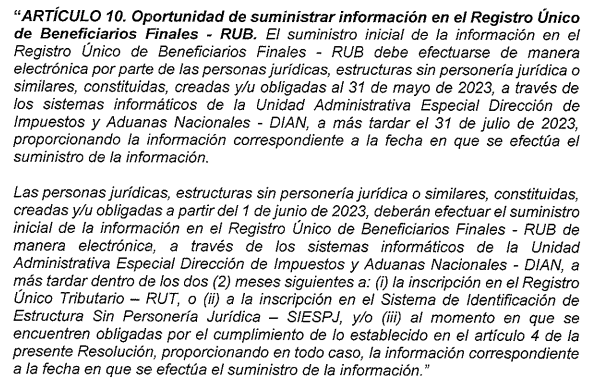

Article 4 of Resolution 164 of December 27, 2021 establishes the parties required to provide information in the RUB; Article 8 defines the content of the information to be provided; and Article 10 established the schedule for sending the requested information to the DIAN as follows: legal entities, structures without legal personality or similar structures created before January 15, 2022 had to submit the information no later than September 30, 2022. Legal entities, structures without legal personality or similar structures created on or after January 15, 2022 had to submit it no later than two months after registration in the RUT or SIESPJ.

Schedule modification:

Resolution 1240 of September 28, 2022 modified Articles 10 and 13 of Resolution 164 of December 27, 2021, that is, the calendar for providing this information. The schedule was as follows:

Legal entities, structures without legal personality or similar structures created before May 31, 2023 must provide the information no later than July 31, 2023.

Legal entities, structures without legal personality or similar structures created on or after June 1, 2023 must provide it no later than two months after registration in the RUT or SIESPJ.

| Creation date | Submission deadline |

|---|---|

| Before May 31, 2023 | Until July 31, 2023 |

| As of June 1, 2023 | Two months after creation |

For all of the above, this obligation should be addressed in a timely manner to avoid the penalties established in Article 20 of Resolution 164 of December 27, 2021, in accordance with Articles 631-6, 651 and 658-3 of the Tax Code.

Remember that to carry out this procedure, obligation 55 must first be included: Beneficial Owner Reporter — legal entity, structure without legal personality or similar structure required to report Beneficial Owners (Article 631-6 of the Tax Code).

For greater clarity on the subject, the DIAN made information available on:

Regulations for the Single Registry of Beneficial Owners (RUB).

Practical tools for the Single Registry of Beneficial Owners (RUB).

General information about the Single Registry of Beneficial Owners (RUB).

If this information helped you, remember to visit us and share your opinion.If you require our advice, contact us at:.

310 558 91 17 - 313 821 48 03

If you need more information, advice or guidance, request an appointment and tell us about your case so we can review the next step.