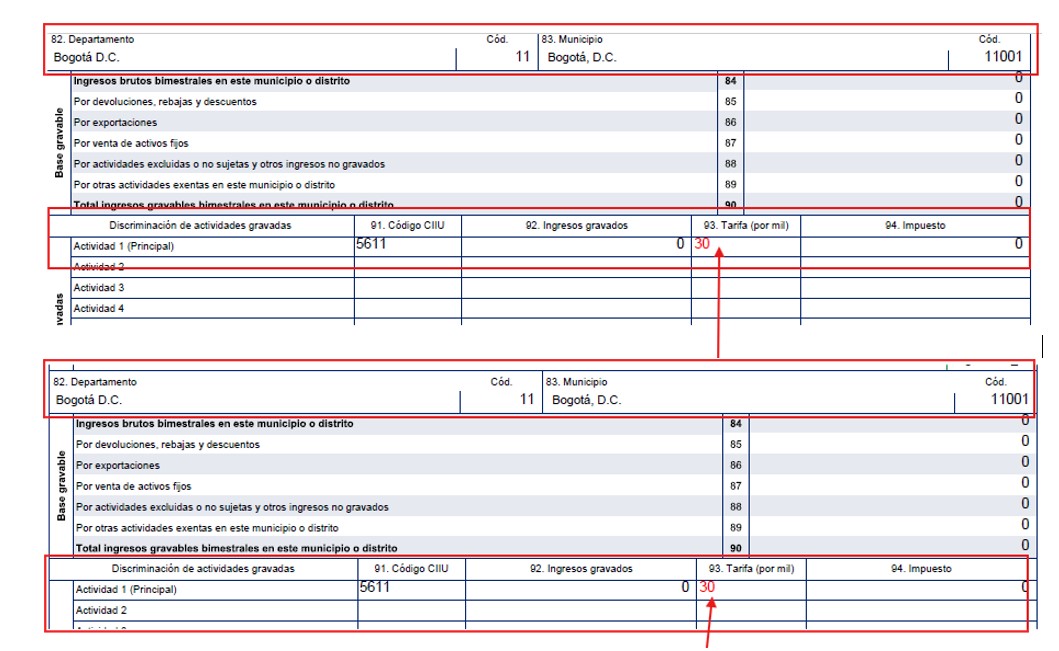

National Consumption Tax (INC)

- Details

- Category: Tax advisory

- Hits: 29

Accounting Bogotá

National Consumption Tax (INC)

Restaurants, cafés, fruit shops, bakeries, fast-food outlets, bars, taverns and nightclubs have a defined regime for value added tax. These activities are generally not required to charge VAT, except in specific cases, but are subject to the National Consumption Tax (INC).

Key information

The simplified and ordinary INC regimes also apply to them. In both cases, those carrying out these activities have obligations, and non-compliance leads to penalties. Many of these businesses fail to comply with minimum legal operating requirements and are exposed to possible fines or penalties. By formalizing your business, you gain an advantage over others because you can focus on growth without fear. Proper classification under the correct regime ensures normal development of activities without creating additional burden.

With our advice, we identify whether you fall under the ordinary or simplified regime of the National Consumption Tax (INC), clearly explaining the advantages and disadvantages in each case and proposing viable alternatives. We always seek compliance with tax regulations while also reducing costs to the maximum extent legally permitted in pursuit of a fair balance.